Analyst Survey: Growth Will Continue to Slow in 2026, but the Ruble Remains Strong

Author: Klaus Dormann

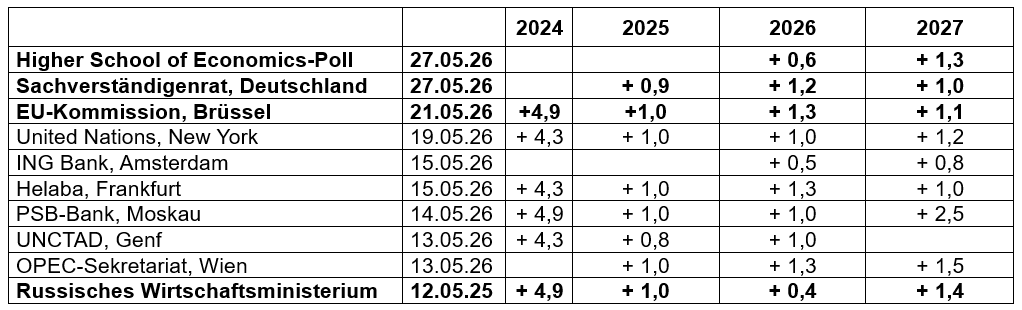

On May 12, the Russian government lowered its forecast for this year’s Russian economic growth from 1.3 to 0.4 percent. However, a few days later, the European Commission (+1.3%) and Germany’s “German Council of Economic Experts” (+1.2%) published significantly higher forecasts for 2026.

“Analysts” at banks and institutions apparently consider the government’s low forecast to be more realistic. In any case, Russian and international experts surveyed by the Economic Research Institute of Moscow’s “Higher School of Economics” from May 18 to 27 now expect economic growth this year to be similarly weak as the government does. They lowered their average forecast for this year’s real gross domestic product growth to 0.6 percent. In February, they had still anticipated an increase of 0.9 percent.

The analysts’ average forecast for growth next year also largely aligns with the government’s assessment. Analysts expect GDP growth to accelerate to 1.3 percent in 2027. The government expects economic growth to pick up to 1.4 percent by then. The European Commission and the German Council of Economic Experts, however, do not forecast an acceleration for next year, but rather a slight decline in the growth rate.

GDP Forecasts for Russia 2024–2027

Year-over-year change in real gross domestic product, in percent

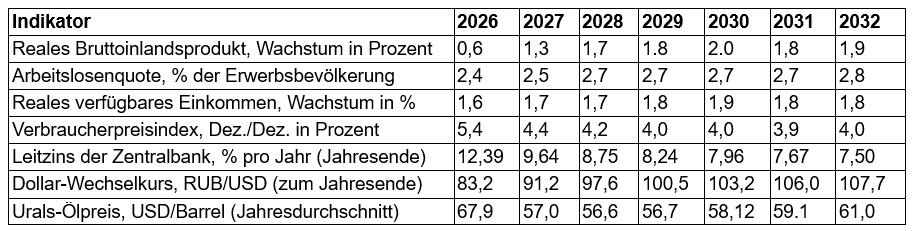

HSE Survey: The Economic “Slowdown” Will Barely Reduce Inflation in 2026

The results of the latest analyst survey listed by the Higher School of Economics in the table below show that, despite the continued slowdown in economic growth, the experts surveyed expect an inflation rate that is, on average, barely lower (5.4%) than that reached in December 2025 (5.6%). By comparison, the Central Bank’s forecast puts the inflation rate at the end of 2026 in a range of 4.5% to 5.5%.

The key interest rate, which was most recently lowered to 14.5% on April 24, is expected to be reduced by a total of about two additional percentage points by the end of the year, according to the HSE consensus forecast. On average, analysts then expect a key interest rate of around 12.4 percent.

HSE Consensus Forecast for 2026–2032

(Expert Survey, May 18–27, 2026)

Higher School of Economics, S.V. Smirnov: Consensus forecast by the Development Center Institute, May 27, 2026

The sharply appreciated ruble will depreciate noticeably by year-end

The Russian ruble has appreciated significantly against the U.S. dollar since early 2025. Most recently, one dollar cost only about 71 rubles. It is thus at its strongest level since early 2023.

However, the HSE survey found that experts now expect the ruble to depreciate significantly by the end of 2026. They anticipate that by year-end, one U.S. dollar will cost around 83 rubles.

Economic “Downturn,” but Currency “Upturn”

Headlines regarding the Russian ruble’s appreciation to date have been piling up in recent weeks. No wonder: the annual growth of the Russian economy already slowed last year from 4.9 percent to just 1.0 percent. For the current year, the majority of experts now expect even less growth. At the same time, however, the Russian ruble has gained significant value against both the U.S. dollar and the Chinese yuan. Fewer and fewer rubles are needed to purchase a unit of foreign currency. This makes Russian imports, which must be paid for in foreign currency, “cheaper.”

How does this all fit together? “Normally,” the equation is: weak economy = weak currency. Why is the ruble so strong, even though it is in less demand than before? After all, many countries have drastically reduced their trade with Russia because it has been hit with sanctions due to the war in Ukraine. Numerous Western companies have left the country. Foreign investment has plummeted. Furthermore, a large portion of Russia’s foreign trade is no longer conducted in rubles. China has been Russia’s largest trading partner for 16 years, and the Chinese yuan is the most important currency in Russian foreign trade (see also IFW Kiel).

The English-language channel “Joe Blogs” analyzed these and other questions regarding the ruble’s performance in a video on May 20. “Joe Blogs” is run by a former financial analyst and management consultant. Below is a summary of his analysis.

How the ruble has performed against the U.S. dollar

Over the past 10 years, the ruble’s exchange rate remained relatively stable for a long time within a range of about 60 to 70 rubles per U.S. dollar. In 2020—during the COVID pandemic and as oil prices plummeted—the ruble weakened: The exchange rate rose from around 62 rubles per dollar before the COVID crisis to about 80 rubles at the peak of the pandemic. This is a sign of how vulnerable the Russian economy is to shocks in global energy markets.

The ruble’s depreciation was even more severe four years ago in 2022, following the invasion of Ukraine. At that time, initial sanctions were imposed and Russia’s foreign exchange reserves were frozen. Within Russia, many feared a severe financial crisis with bank failures. At its peak, the exchange rate reached around 120 rubles to the U.S. dollar.

Ruble per US Dollar over the last 5 years

Trading Economics: Russian Ruble, May 29, 2026

However, after this initial slump, the ruble recovered quickly. By mid-2022, it had even reached an exchange rate of about 50 rubles per U.S. dollar—its strongest level in about ten years. However, it subsequently weakened significantly again until around the end of 2024. Since then, the ruble has appreciated significantly. It is now stronger than it has been since early 2023.

This was unexpected: “Normally,” currencies appreciate when an economy is booming. Foreign capital then flows into the country, increasing global demand for that currency. In Russia, however, economic growth slowed sharply as early as last year.

What interest does the Russian government have in a strong ruble?

Historical experience shows that countries under sanctions often benefit from a currency devaluation. In Russia, however, the ruble is appreciating despite the sanctions. What explanations are there for this? Does the Russian government have an interest in a strong ruble?

The first explanation is the government’s interest in more stable prices. Russia has been battling a very high inflation rate for quite some time. One of the quickest ways to curb imported inflation is to strengthen the country’s own currency. After all, a strong ruble makes imports cheaper. Politically, this is of great significance. If the ruble collapses, domestic prices will skyrocket. The Russian population will then feel the impact of inflation in very sensitive areas such as food, electronics, cars, medicines, and other consumer goods. From the government’s perspective, it is therefore likely very important to maintain a strong currency.

A second aspect, from a political perspective, is that a strong currency has a psychological impact. Headlines celebrating the ruble as the “strongest currency” then appear—as they have in recent weeks. The government can present this as proof that Russia is resilient and that the sanctions have come to nothing. An appreciation holds enormous propaganda value for the government both domestically and internationally. Currencies have symbolic significance: a strong currency is equated with national strength.

A third possibility is that the government is concerned with the stability of the financial system. The Russian banking system has been under enormous pressure since the sanctions began. A weak ruble carries the risk of triggering capital flight, which could lead to panic and instability in the banking sector. If the authorities keep the exchange rate relatively strong, they can expect to maintain confidence in the financial system.

What are the disadvantages of a strong ruble?

However, a rise in the ruble’s value also has serious drawbacks: the stronger the currency becomes, the more difficult it is for exporters. And at its core, the Russian economy remains an export-oriented commodity economy. It is based on oil, gas, metals, and other raw materials. These are the sources of the country’s revenue.

If the revenues of these exporters come under pressure due to the ruble’s appreciation while their costs continue to rise as a result of inflation and war-related burdens, the profitability of these companies ultimately suffers massively. But if corporate profitability declines, so do the government’s tax revenues. And if tax revenues fall while military spending remains at extremely high levels, the Russian state’s finances come under increasing pressure.

“Joe Blogs”’ conclusion: The ruble exchange rate is a “managed exchange rate”

Based on these considerations, “Joe Blogs” draws the following conclusions, among others:

What we are seeing in Russia “is not a truly strong currency backed by a strong economy, but a managed exchange rate used as a political and financial tool. … The reality is that, according to many analysts, the ruble would likely trade at a significantly weaker level than it does currently in a free and fully open market.”

“Joe Blogs” emphasizes that the ruble exchange rate does not form in a “normal economic environment.” Russia is an economy characterized by sanctions, capital controls, restrictions on capital movements, massive state intervention, and a growing dependence on China.

Recommended reading:

Forecasts:

- 1Prime.ru. Svetlana Medvedeva: “Better than us.” How Russia surprised the EU. European Commission’s Spring Forecast for the EU, Russia, and Germany; May 28, 2026

- Higher School of Economics, S.V. Smirnov: Consensus forecast by the Development Center Institute, May 27, 2026; Archive of issues

- Kommersant on UNCTAD forecasts: Trade will slow down along with GDP. Forecast by the United Nations Conference on Trade and Development (UNCTAD), May 25, 2026

Foreign Trade: Ruble Exchange Rate, Sanctions, and Trade with China:

- Alfa Bank; Vasily Karpunin, Head of the Information and Analysis Department at Alfa Investments; Economy and Trends: What to expect from the ruble in June? May 29, 2026

- Tagesschau.de; Angela Göpfert: Ruble Rally: Why the Strong Ruble Harms Putin, May 28, 2026

- The Riddle; Vladislav Inozemtsev: The Pivot to the East Has Succeeded. But There Are Nuances. How partnership with China has turned Russia into its technological vassal; May 27, 2026

- Kommersant: Shokhin spoke about the impact of the ruble’s appreciation on federal budget revenues, May 27, 2026

- Alfa Bank; Anastasia Stepantsova, Economy and Trends: The ruble has stopped appreciating. Has the trend reversed? May 26, 2026

- Kommersant: Trade will slow down along with GDP. Forecast by the United Nations Conference on Trade and Development (UNCTAD), May 25, 2026

- Alexander Kolyandr; Senior Fellow at the Center for European Policy Analysis (CEPA): The British and US Sanctions That Quietly Aren’t. US and UK sanctions relief aimed at easing domestic consumer pressures also transfers billions into Putin’s war chest, at Ukraine’s expense, May 22, 2026

- Joe Blogs, Video: Russian Ruble Crisis. In this video, we examine the mysterious rise of the ruble and ask whether it is now being actively managed behind the scenes, May 20, 2026

- russland.capital: Russia and China: Lots of Talk About Partnership, but Beijing Is Calculating Coolly; May 24

- Alfa Bank; Arseniy Anatolyev: The ruble exchange rate has peaked, May 22, 2026

- wallstreetONLINE; Ingo Kolf: Revenues are pouring in. Russia is profiting massively: The secret winner of the Middle East war, May 21, 2026

- Frankfurter Rundschau; Marcel Reich: Putin’s oil via detours: Why London is backing down on Russia sanctions, May 21, 2026

- BANKNN:RU: The dollar exchange rate fell below 70 rubles for the first time since 2023, May 21, 2026.

- Sergei Guriev; CNBC Interview: Guriev: Russia needs a pipeline to China; Sergei Guriev, dean of London Business School, discusses the impact of rising oil prices on Russia’s economy and the country’s relationship with China, May 19, 2026

- CNBC; Holly Ellyatt: Putin in Beijing: 3 things Russia needs from China, May 19, 2026

- Vedomosti+; Ksenia Kotchenko, Anastasia Boyko: The Russian currency reaches its strongest level this year, May 19, 2026

- Inosmi.ru: The ruble has appreciated against the dollar more than ever before: What’s behind this? BZ: Reliable mechanisms of the Central Bank of Russia contributed to the ruble’s strengthening. May 20, 2026; Original article: Berliner Zeitung, Liudmila Kotlyarova: Ruble gains the most against the dollar worldwide: What’s behind this? The ruble lost significant value after the start of the Iran war. Now, according to Bloomberg, it is the biggest global winner against the U.S. dollar. How is this possible? May 19, 2026

- Inosmi.ru: The ruble is performing better than all other currencies: Russia benefits from the oil boom caused by the Iran war: Bloomberg original article; May 19, 2026

- Alfa Bank, Arseniy Anatolyev: The Ministry of Finance’s currency purchases were unable to stop the exchange rate from appreciating, 05/15/26

Economic data: Industrial production in April:

- Finam.ru; Pavel Paevsky, Head of the Macroeconomic Credit Analysis Department at RSHB Asset Management: Economic statistics from recent weeks have not changed the overall picture. Neither here nor there; May 28, 2026

- FocusEconomics: Russia Industrial Production April 2026, May 27, 2026

- Kommersant; Artem Chugunov: Industry is on an uncertain path, May 28, 2026

Politics and Economy in Russia; Overall Economic Development:

- Business City Petersburg, Anton Taranukha: GDP Forecast, Shochin’s Promotion, and Preferential Mortgages: The Most Important Economic Events in May, May 29, 2026

- russland.capital: Russia’s Business Association Warns Government: Don’t “Squeeze the Economy Too Hard,” May 26, 2026

- bne Intellinews; Ben Aris: CBR Governor Nabiullina’s term expires next year and the list of potential replacements is short – The Bell, May 25, 2026

- Fortune; Jason Ma, Weekend Editor: Russia’s economy is much worse than it seems, and ‘elites are increasingly alarmed’ as an alternative GDP gauge shows a massive contraction. In a New York Times op-ed on Wednesday, Foreign Minister Maria Malmer Stenergard cautioned the West against overestimating Russia and said the economy is more fragile than it appears, May 24, 2026; Gazetaexpress.com: Maria Malmer Stenergard: Russia’s economy is more fragile than it seems. May 25, 2026

- en.ara.cat; Leandre Ibar Penaba: Russia abandons economic optimism. Sanctions, Ukrainian bombings, labor shortages, and inflation push an economy geared toward the war effort to the limit, May 25, 2026; Alexander Kolyandr, CEPA: Europe’s Edge: Russia Settles for Stagnation. The Kremlin’s own forecasters now admit what they long denied: the war economy has run out of steam, 04/20/26

- russland.capital. Natalya Zubarevich: Russia’s economy is slipping—but not into a crash; May 25, 2026; see also:

Republicmag.io; Egor Senchin: “We have to survive this madhouse somehow.” Natalia Zubarevich and her colleagues on how the Russian economy can survive in 2026; 05/22/26;

66.ru: “They overreacted toward small businesses.” – Economist Natalia Zubarevich on who will be hit the hardest. May 12, 2026;

prufy.ru; Rustam Nabiullin: “They have Tatneft.” Natalia Zubarevich on the industrial decline of Bashkortostan and the reasons for its “eternal” lag behind Kazan; May 20, 2026 - Gazeta.ru: Growth Under Constraints: How the Private Sector Became a Pillar of the Russian Economy in the Age of Sanctions. Russia’s GDP grew by 1.8% in March; May 25, 2026

- Maeil Business: Trade surplus jumps 175% in March. Market outlook optimistic despite Russia’s negative growth, May 23, 2026

- Alexander Kolyandr, CEPA: Europe’s Edge: Russia Settles for Stagnation. The Kremlin’s own forecasters now admit what they long denied: the war economy has run out of steam, May 20, 2026

- russland.capital: Reshetnikov calls for room to lower interest rates and increase economic efficiency, May 20, 2026

- Inosmi.ru: No, the Russian economy is not on the verge of collapse. FP: There is no reason to talk about a possible collapse of the Russian economy. May 23, 2026; Original article in Foreign Policy: No, Russia’s Economy Is Not About to Collapse. The war with Ukraine has slowed growth, but Moscow remains stable. By Cameron Abadi, a deputy editor at Foreign Policy, and Adam Tooze, a columnist at Foreign Policy and director of the European Institute at Columbia University; May 21, 2026; Foreign Policy podcast “Ones and Tooze”: Adam Tooze on Russia’s economic slowdown, May 15, 2026