Is Russia a “war economy”? What do international experts say?

Author: Klaus Dormann

Reports of preparations for negotiations to end the war in Ukraine are mounting. What impact would a ceasefire have on the development of the Russian economy? It is often argued that the Russian economy has now become a “war economy” that would fall into recession if a peace agreement were reached. On the other hand, it is pointed out that high military spending has not only led to a sharp rise in production so far. It has also brought benefits to Russian citizens. Real wages have risen sharply.

What do experts say about this? Below are some insights into the trend of Russian military spending and comments by Sergei Guriev, Janis Kluge, and Jacques Sapir on the trend of military spending in the context of Russia’s overall economic development.

SIPRI estimates on the rise in Russian military spending

The Stockholm International Peace Research Institute (SIPRI) publishes annual studies on global trends in military spending. The following Statista chart on the trend in Russian military spending uses data from the SIPRI Fact Sheet “Trends in World Military Expenditure, 2024,” published in April 2025. The chart shows that Russia’s military spending as a share of its gross domestic product roughly doubled over the course of the first three years of the war in Ukraine.

Statista; J. Rudnicka: Russia’s Military Expenditures Through 2024, Nov. 26, 2025;

“Stockholm International Peace Research Institute”: SIPRI Fact Sheet, April 2025

In 2021, the year before the war began, military spending accounted for 3.6 percent of GDP. By 2024, this share had reached 7.1 percent (blue bars).

Russian military spending rose to approximately $149 billion in 2024 (black line). In 2021, it had amounted to only about $66 billion. Military spending has thus more than doubled. In US dollars, it has risen even more sharply in percentage terms since 2021 than its share of GDP has increased.

The figure clearly shows that the level of Russian military spending in U.S. dollars is highly dependent on fluctuating exchange rates due to the conversion of rubles to U.S. dollars at current exchange rates. As a result, Russia’s military spending in U.S. dollars fell significantly from 2013 to 2015 due to exchange rate fluctuations. At the same time, however, the share of military spending in gross domestic product rose significantly (for further information on methods for measuring military spending, see: Prof. Dr. Richard Reichel, FOM University of Applied Sciences Essen: On Par with Russia: What Military Resources Are Needed? Wirtschaftsdienst, April 2025)

How will the share of military spending in GDP develop in 2025 and 2026?

According to a SIPRI study published in April 2025, Russian military spending is expected to rise to 7.2 percent of GDP in 2025 (Julian Cooper: Preparing for a Fourth Year of War: Military Spending in Russia’s Budget for 2025, April 2025).

According to Aleksandr Kolyandr, military spending is also expected to remain at around 7 percent of GDP in 2026. The “Senior Fellow” at the Washington-based “Center for European Policy Analysis” reports in an article on the Russian government’s budget planning:

“In 2026, the defense budget is set to decline for the first time since the invasion of Ukraine, from 13.5 trillion rubles ($161 billion) to 12.93 trillion rubles. This is roughly in line with last year’s plan, which called for spending of 12.8 trillion rubles.

However, spending on national security and law enforcement will rise from 3.56 trillion rubles in 2025 to 3.91 trillion rubles in 2026.

As a result, combined spending on defense and national security will remain at a record level of just under 40% of federal spending and about 7% of GDP.”

Sergei Guriev: Military spending accounts for about 10 percent of GDP

Sergei Guriev is Dean and Professor of Economics at the London Business School. The former rector of Moscow’s New Economic School emigrated in 2013. Among other roles, he served as Chief Economist at the European Bank for Reconstruction and Development in London.

On the Financial Times podcast “The Economics Show” in mid-February, Guriev also commented on the question of what share of total economic output Russia currently spends on defense and security. If you add these two items together, it would amount to around 10 percent of GDP, according to Guriev. The actual figure, however, could be even higher.

At the same time, however, Guriev emphasized that no one is claiming that today’s Russia is as heavily militarized as the former Soviet Union. Some estimated defense and security spending in the Soviet Union at up to 20 percent of GDP.

The end of the Cold War and the drastic demilitarization of the Soviet Union had a severe impact on the entire Russian economy at the time, because the defense sector accounted for such a large portion of the Soviet economy. The recession in Russia in the early 1990s was a severe shock. Employees of the “defense industry” had to be painstakingly retrained.

Regarding occasional fears that President Putin does not want to negotiate peace in Ukraine because he fears a post-war recession, Guriev said in the FT podcast:

“Russians know how to live in a peaceful economy. It wasn’t that long ago, and the military economy is probably only half as large today as it was in Soviet times. And Russia is a market economy. Therefore, the economy will adapt more easily. … Some claim that all of Russia is working for this war, that Russians support it because they benefit from it. I think that’s an exaggeration.”

Source: Financial Times podcast “The Economics Show”; Martin Sandbu talks to Sergei Guriev, dean of London Business School: The real Russian economy. With transcript, 02/18/25

Sergei Guriev: Economic problems are not yet forcing President Putin to back down in the war in Ukraine

In October, Guriev commented on Russia’s growing economic problems in an article for “Project Syndicate,” which was also published by the Austrian newspaper “Der Standard.” However, these will not yet lead to a change of course by President Vladimir Putin in the war in Ukraine, Guriev believes.

Below is a summary of some of Guriev’s remarks on the current state of the Russian economy, which he also refers to as a “war economy”:

Significantly lower growth, persistently high inflation, rising budget deficit

Even the most optimistic forecasts predict that Russian growth this year will be only about one percent—a significant decline from 4.3 percent in 2024 and 4.1 percent in 2023. Despite this downturn, inflation remains a problem.

President Vladimir Putin also faces challenges on the fiscal front. In the first eight months, tax revenues from the oil and gas sector fell by about 20 percent compared to the previous year, causing reserves in the sovereign wealth fund to dwindle.

Russia’s budget deficit is expected to rise to 2.6 percent of gross domestic product by the end of the year. By U.S. or European standards, the deficit is low. However, it is problematic for a country that has been cut off from borrowing on the international capital market as punishment for its invasion of Ukraine.

Since Putin knows he will run out of money in less than a year, he has just announced a budget that includes significant tax hikes. These will further strain the economy.

However, Russia’s economic situation is “not yet catastrophic”

The Russian economy may be stagnating, but it is not collapsing. And with a working-age population of more than 72 million people, Putin can still recruit about 30,000 soldiers per month by paying men from Russia’s poorest regions ten to twenty times their average wage.

These factors and his apparatus of repression likely convinced Putin that he has the means to keep his war economy running and to suppress discontent in the country for as long as necessary.

In the short term, Putin has sufficient resources to maintain order at home and finance his army’s slow advance in Ukraine. Yes, this comes at the expense of spending on education, healthcare, innovation, and infrastructure. But for Putin, progress on the battlefield is a better investment in Russia’s future: it means he will have a stronger hand when the time comes to reach an agreement.

Source: Sergei Guriev; commentary in “Der Standard”: How Russia Is Suffering Under Putin’s War Machine; Project Syndicate, Oct. 20, 2025; see also on the development of the Russian economy: Wall Street Journal video: How Much Longer Can War Prop Up Russia’s Economy?, 5 min., with Guy Anderson, Head of Defense Markets, Janes; Aug. 5, 2025

Janis Kluge: Russia Has Not Yet Entered a “War Economy”

Dr. Janis Kluge, a Russia expert at the Berlin-based German Institute for International and Security Affairs (SWP), still does not view the Russian economy as a “war economy.” In an interview on the podcast “Thema des Tages” by the Austrian newspaper “Der Standard” on November 11, Kluge summarized Russia’s economic system as follows:

The Russian economy is a “special market economy,” a market economy with certain restrictions. At its core, however, prices, private companies, and the motive of profit maximization play a very, very significant role in the Russian economy. This naturally gives the economy a certain resilience. The Russian economy is largely a private economy. However, it has a very dominant state sector, especially in the energy sector.

I would still not describe Russia’s economy as a “war economy.” The changes are not yet significant enough for that. Russia’s military spending is indeed very high. About 8 to 10% of the gross domestic product is spent on the military. An incredible number of people are being recruited for the war, but also for the defense industry. So the war is also very clearly felt in the labor market.

The Russian economy is likely more of an economy that is slowly being mobilized for war, but has not yet fully transitioned into a war economy.

A large part of the population is simply ignoring the war

The war and its consequences are indeed becoming a burden. The sharp rise in inflation in recent years is very clearly attributable to war spending, which is forcing the central bank to impose extremely high interest rates and thereby stifle the economy.

Overall, however, it remains possible for many people in Russia across various professions and sectors to ignore the war. A large part of Russian society simply turns a blind eye to this war.

Putin’s power is based on the fact that people can ignore the war.

Kluge: Parts of the population have benefited greatly from war spending

The defense industry, of course, has benefited from war spending, having suffered greatly after the end of the Soviet Union. Russia’s industrial regions have thus also benefited greatly from war spending.

At least certain segments of the Russian population have also benefited greatly from war spending. War spending includes soldiers’ salaries, “recruitment bonuses,” and compensation for the families of fallen soldiers. These cash benefits from the state go to households that were previously rather poor. They contribute to an overall rise in incomes in Russia. The war-induced labor shortage is also having an effect in the form of rising wages.

However, the population does not actively support the war

If the economy now runs into trouble,

if gasoline becomes scarce, if inflation skyrockets,

if the state has to raise taxes or cut spending,

then the war will of course suddenly become very tangible for everyone.

Then it will also become clear that the population does not really understand this war. There are few truly ardent supporters of this war among the Russian population, while the regime is waging the war with relative fanaticism. The population simply accepts the war, but does not actively support it.

This gap between the Russian regime and what the population actually thinks about the war will become much more palpable once the cost of the war becomes clearly visible to everyone. Economic developments play a central role in this.

Source: Janis Kluge, German Institute for International and Security Affairs (SWP), in the “Der Standard” podcast “Thema des Tages” in an interview with Schold Wilhelm: Is Russia’s economy on the verge of collapse? 34 min., Nov. 11, 2025

Jacques Sapir: Russia has too high interest rates and too few workers

Professor Jacques Sapir (born 1954) teaches at the “School of Economic Warfare” in Paris. He was Director of Research at the École des Hautes Études en Sciences Sociales (EHESS) in Paris. Sapir is, among other things, a member of the Russian Academy of Sciences.

In November, Sapir visited the “Danube Institute” (Institute for Danube Region Studies and European Integration Research) at the German-language Andrássy University of Budapest (AUB), which is funded by the Federal Republic of Germany, the Free State of Bavaria, the State of Baden-Württemberg, Austria, and Hungary. “Hungarian Conservative” published an interview by Tamás Maráczi with Sapir (also available as a video) on the following questions:

0:44 – How much longer can Russia sustain the war in Ukraine economically?

4:22 – Is the Russian economy resilient, or does it face serious problems?

8:36 – Are there long lines at Russian gas stations?

11:50 – Are there signs of runaway inflation or a recession?

14:01 – How is the Russian middle class feeling the effects of the war?

17:46 – When might a tipping point be reached where living standards decline?

22:00 – What are the long-term vulnerabilities of the Russian economy?

24:46 – How much does Russia spend on defense?

26:50 – Why hasn’t Russia won this war in a spectacular fashion?

32:05 – Are the Baltic states’ and Poland’s fears of Russia justified?

33:45 – What could be the most realistic outcome of this war?

In the interview on the development of the Russian economy, Sapir summarizes the following points, among others:

Russia is an “economy at war,” but not a “war economy”

Military spending accounts for between 6.5 and 7 percent of Russia’s GDP.

Russia’s defense industry has developed so far without adversely affecting the civilian sector. This is precisely the key difference between an “economy at war” and a “war economy.” Russia still has a civilian industry that is developing independently. This model is sustainable over the long term. At its current growth rate, Russia can continue its war efforts for five or ten years—perhaps even indefinitely.

One problem facing the economy is the shortage of skilled workers

The shortage of skilled labor remains a problem for Russia. The unemployment rate stands at 2 percent, which is actually very low. There is therefore a labor shortage that should be addressed through increased labor productivity and immigration.

Russia has no problem exporting its energy. We know that oil and gas are exported largely to China and India.

The budget deficit is also not a problem. It will reach around 3 percent in Russia, which corresponds exactly to the limit prescribed by the EU. For France, a budget deficit of 3 percent is “a miracle.” The deficit in France stands at 5.6 or 5.8 percent of GDP.

The temporary fuel shortage in Russia is related to the fact that Russian refineries traditionally enter a maintenance phase in August and September. While Ukrainian attacks on some refineries are exacerbating the situation this year, the fuel shortage is a short-term problem.

Sapir: The central bank has raised the key interest rate far too much

Before the war, inflation was already around 6 percent. In December 2024, it stood at 10.5 percent. Due to the war, inflation has risen by about 4.5 percentage points. Of that, roughly half—about 2 percentage points—was likely attributable to the sanctions. The sanctions did not prevent imports, but merely made them more expensive.

The central bank raised the key interest rate far too high. In January 2025, the nominal interest rate was 21 percent with an inflation rate of 10.5 percent, implying a real interest rate of 10.5 percent—a figure that was far too high. Real interest rates should have been raised to only 4 or 5 percent.

The following chart from DekaBank shows the development of the annual inflation rate and the annual key interest rate since early 2022.

DekaBank: Emerging Markets Trends:

Russia: No Concessions in Negotiations Despite New Oil Sanctions, 11/06/25

Sapir: Real wages have risen sharply

For the Russian “upper class,” the war has had no impact so far and will continue to have none.

For the “upper middle class”—which should not be equated with the upper class—the war does, however, have consequences, primarily because progressive income taxation particularly affects the “upper middle class.” The “upper middle class” makes up only 10–12 percent of the Russian population, which is why their interests are largely neglected by the government.

For the rest of the population, however, the war has had little impact. In fact, it has even led to a significant increase in real wages (+10% in 2023, +7% in 2024, and around +5% this year). Employees in the retail sector benefited less from these wage increases than those in industry.

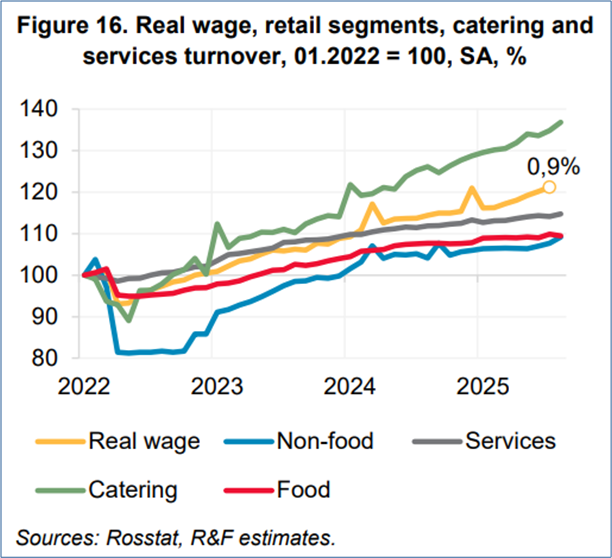

Central Bank chart on real wage trends since early 2022

Sapir’s assessments of real wage trends are illustrated by the following chart from the Russian Central Bank in its latest economic report, “Talking Trends.” It shows the rise in real wages and key areas of private consumption from early 2022 through August 2025 (real wages through July 2025).

It is evident that real wages have risen by approximately 20 percent during the war years from January 2022 to July 2025 (yellow line). In July 2025, real wages rose by 0.9% on a seasonally adjusted basis compared to June.

Real sales in the “Catering/Food Service” sector rose particularly sharply by a good third from January 2022 to August 2025 (green line). At the same time, real sales in the “Services” sector grew by around 12 percent (gray line). Real sales in the retail sector showed the weakest growth. In August 2025, they were only just under 10 percent higher than in January 2022 in both the “Food” sector (red line) and the “Non-food” sector.

Real wages have risen by about 20 percent since early 2022 (yellow line)

Development of real wage and

real retail sales indices (food, non-food),

in the restaurant industry, and in services, seasonally adjusted (Jan. 2022=100)

Russian Central Bank: Talking trends, Oct. 14, 2025

Recommended reading:

- CMASF: Industrial production trends in October 2025, Nov. 28, 2025

- Politcom.ru; Marina Voitenco: Business activity and prices: mixed dynamics, Nov. 28, 2025

- Japan Times: Russians are starting to feel real economic pain from Putin’s war, Nov. 27, 2025

- NZZ, Dominik Feldges: Pay cuts, furloughs, layoffs: The Russian economy is paying a high price for the war. Russia is in a slump. 11/27/25

- Frank Media, Natalia Trapeznikova: Wage growth has not led to an increase in Russians’ well-being, 11/27/25

- Statista; J. Rudnicka: Russia’s military spending through 2024, Nov. 26, 2025

- Salto; Monika Psenner: Global military spending is rising, 06/03/255

- Forbes.com, Ariel Cohen: Cracks in Russia’s War Economy, 11/25/25

- Military & History with Torsten Heinrich: Russia’s Economy is IMPLODING! Video, 30 min., Nov. 23, 2025

- Crisis Watch, Video: Putin’s $207 Billion GAMBLE: Why Russia’s Economy is Headed for Disaster, 17 min., Nov. 16, 2025

- Express, Martin Gätke: “Ticking Time Bomb”: Is Russia Now Facing Collapse?, 11/25/25

- Interfax.ru: The Central Bank expects inflation to return to a low level in 2026. This will make it possible to lower the key interest rate to an acceptable level, said Alexey Zabotkin, Deputy Chairman of the Bank of Russia, Nov. 24, 2025