Russia's 1% growth rate is not expected to rise to 1.5% until 2027

Author: Klaus Dormann

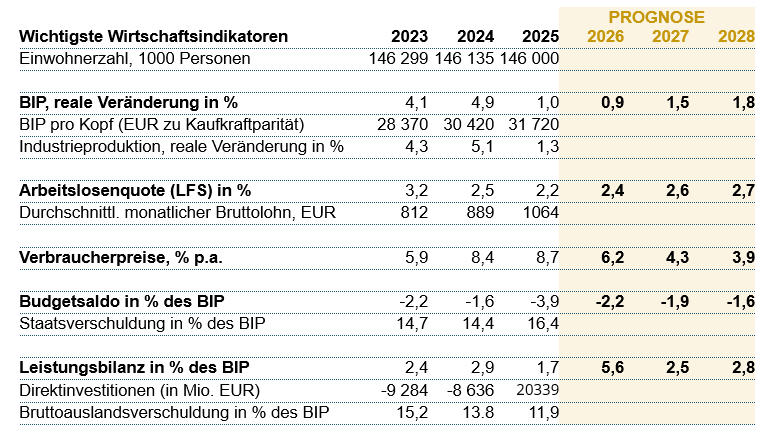

According to the Russian Ministry of Economic Development, Russia’s gross domestic product in the first quarter of 2026 was 0.3 percent lower than a year ago. In light of the weak production trend at the start of the year, the “Vienna Institute for International Economic Studies” (wiiw) has now lowered its forecast for this year’s growth in the Russian economy from 1.2 percent to just 0.9 percent. This would make it slightly lower than in 2025. Last year, growth slowed from 4.9 to 1.0 percent. However, the wiiw still expects growth to accelerate to 1.5 percent in 2027.

Is Russia now even sliding into a “recession”?

In addition to the wiiw, other institutes and banks have lowered their forecasts for this year’s growth in the Russian economy. The Moscow-based “Center for Macroeconomic Analysis and Short-Term Forecasting (CMASF)” nearly halved its monthly updated growth forecast for 2026 at the end of April. It now expects GDP growth of only 0.5 to 0.7 percent this year. In March, it had still forecast economic growth of 0.9 to 1.3 percent for 2026 (The Moscow Times). Sberbank now expects real GDP growth of only 0.5 to 1 percent for 2026. The previous forecast range from Russia’s largest bank had been 1.0 to 1.5 percent (russland.capital).

According to globalmsk.ru, some analysts believe the Russian economy is already in a “recession” given the 0.3 percent decline in production in the first quarter of 2026 compared to the first quarter of 2025. However, Nikita Maslennikov, a leading expert at the “Center for Political Technologies,” disagrees with this assessment in an interview with globalmsk.ru. In his opinion, Russia is unlikely to see a further decline in real gross domestic product in the second quarter, as “external factors” will play a greater role in the second quarter than they have so far. The rise in energy prices due to the conflict in the Middle East has led to additional oil and gas revenues. These are expected to flow into the federal budget starting in mid-April.

Regarding current economic developments, Maslennikov emphasizes that the 2.3 percent overall increase in industrial production in the first quarter of 2026 is attributable exclusively to the rise in production in the “defense industry.” Production in the civilian sectors of industry was 0.6 percent lower than in the previous year.

Regarding the recovery of consumer demand in the domestic market, he notes that price trends stabilized somewhat in March following the rise in January and February. This slightly increased consumer demand.

wiiw: “Stagnation in Russia Despite Financial Windfall from Iran War”

This is the headline used by the “Vienna Institute for International Economic Studies” (wiiw) for the Russia chapter in the press release accompanying its “Spring Forecast” for 23 countries in Central, Eastern, and Southeastern Europe, published at the end of April. However, the institute does not expect “stagnation” with zero growth in aggregate economic output in Russia in 2026. It is merely lowering its GDP forecast for the current year by 0.3 percentage points to 0.9 percent.

For Russia’s budget, the windfall comes “at exactly the right time”

In its press release, the Vienna-based institute assumes that the Russian state budget, in particular, will benefit from the rise in energy prices:

“The closure of the Strait of Hormuz has brought Moscow unexpected additional revenue from higher oil and gas prices. From Russia’s perspective, this comes at exactly the right time, as it alleviates the strained budget situation. Last year, the budget deficit stood at 3.9 percent of GDP—a fairly high figure by Russian standards. Until the start of the war against Iran, it had looked as though the Russian budget deficit might spiral out of control this year, which is why the government had considered cuts of 10 percent, with the exception of military and social spending.”

“The war with Iran is stabilizing the Russian budget. The longer it lasts and the longer oil prices remain high or rise even further, the more positive the effects will be for Russia; after all, for every dollar the price of crude oil rises, 58 cents flows into the Russian state budget,” says Vasily Astrov, a Russia expert at wiiw.

Russia’s GDP growth benefits “only marginally” from higher energy prices

According to the press release, however, the development of production in the Russian economy is likely to benefit “only marginally” from higher energy prices. The higher revenues would not be channeled into additional spending, but are instead earmarked for reducing government borrowing and paying down the liabilities of energy companies.

Vasily Astrov cites “still-high key interest rates,” insufficient investment in new production capacity, and labor shortages as the main causes of the Russian economy’s weak growth. The high energy prices resulting from the war in Iran would do little to change this. Astrov highlights the political implications of higher energy prices:

“Undoubtedly, the war in Iran is helping President Putin to continue his war of aggression against Ukraine, as it provides him with additional revenue and greater political leeway.”

Russia will drop to near the bottom of the wiiw’s growth rankings by 2027

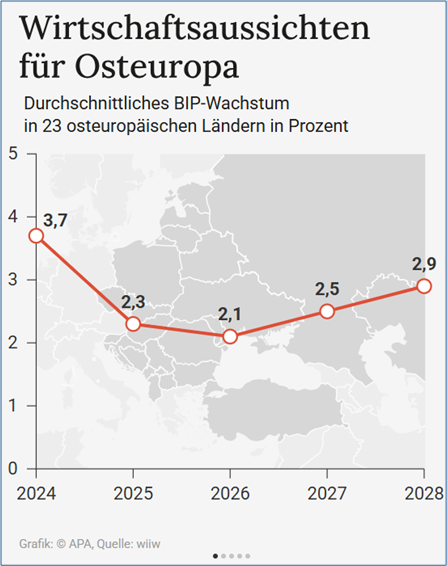

The forecast by the Vienna Institute for International Economic Studies covers a total of 23 countries in Central, Eastern, and Southeastern Europe, including Turkey (see table at the end of the wiiw press release).

In the following figure, these countries are marked in dark gray. The figure shows that, according to the wiiw, economic growth in these countries will decline on average from 2.3 percent in 2025 to 2.1 percent in 2026.

Kronenzeitung: Eastern Europe continues to grow faster than the Eurozone, April 29, 2026

The following two “rankings” for growth rates in 2026 and 2027 cover 12 of the 23 countries in total. The wiiw expects the strongest growth among the selected 12 countries in 2026 and 2027 to be in Turkey (2026: 3.7 percent; 2027: 4.1 percent). Poland will lead the way in growth among the selected Eastern EU member states (blue bars) in 2026 with 3.6 percent. In 2027, Croatia (2.7 percent) is expected to grow slightly faster than Poland (2.6 percent).

Kronenzeitung: Eastern Europe continues to grow faster than the Eurozone, April 29, 2026

Hungary’s economy will grow by 1.6 percent in 2026 and by 1.8 percent next year.

At the bottom of the above ranking for 2026 are the EU member states Romania and Slovakia. Their growth in 2026, at 0.5 percent each, is expected to be even lower than Russia’s growth (0.9 percent).

In 2027, Russia will then slip to the bottom of the ranking of the selected 12 countries—although the wiiw expects Russia’s growth to accelerate to 1.5 percent in 2027. The complete table of forecasts for all 23 countries in the wiiw press release shows that the institute expects only Belarus to have slightly weaker economic growth in 2027 (1.4 percent) than Russia (1.5 percent).

wiiw “Country Overview”: Russia’s growth rises to 1.8 percent by 2028

In its “Country Overview” for Russia, the wiiw notes the following for 2026:

The additional revenue generated by high energy prices resulting from the war in the Middle East has provided much-needed relief for the strained national budget.

They are also likely to have a slightly positive impact on economic growth, which slipped into negative territory at the beginning of 2026.

In the baseline scenario, real GDP growth of 0.9 percent is forecast for this year, followed by an acceleration in 2027 and 2028 due to the expected easing of monetary policy.

Should global energy prices remain high or continue to rise in the longer term, GDP growth will be higher, though inflation will also accelerate.”

Compared to its “Winter Forecast” from January, the wiiw has now lowered its forecast for this year’s real gross domestic product growth from 1.2 to 0.9 percent. It maintained its growth forecast for 2027: It continues to expect growth to accelerate to 1.5 percent next year. The wiiw raised its growth forecast for 2028 from 1.5 to 1.8 percent.

wiiw Country Overview: Russia

wiiw: Country Overview Russia, April 29, 2026

Current account surpluses will be much higher than previously expected

The wiiw has significantly raised its forecasts for Russia’s current account surpluses in light of the current sharp increases in energy and commodity prices. In 2026, the current account surplus will reach 5.6 percent of gross domestic product (previous forecast: 1.1 percent of GDP). According to the new forecasts, current account surpluses in 2027 (2.5 percent of GDP) and 2028 (2.8 percent of GDP) will be roughly twice as high as the wiiw had previously expected.

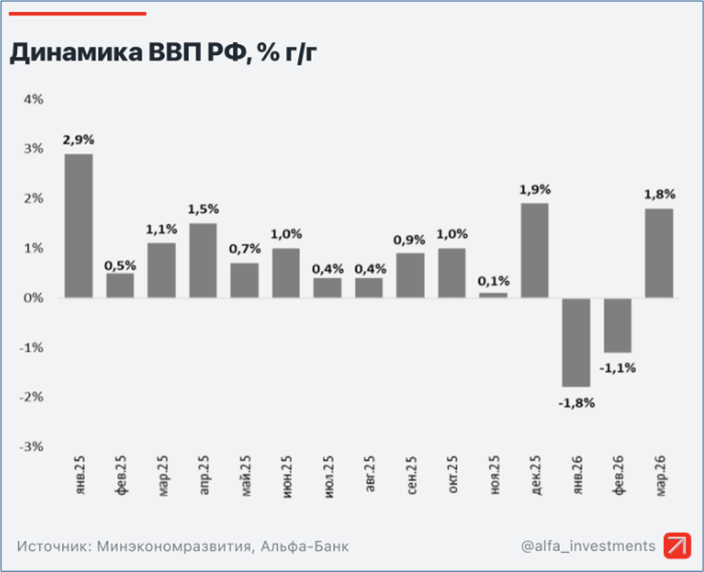

Economic Performance in the First Quarter of 2026: Russia’s GDP Fell by 0.3 Percent

In March 2026, Russia’s gross domestic product rose by 1.8 percent year-over-year, according to the Russian Ministry of Economic Development. However, the increase in March did not fully offset the annual GDP declines in January (-1.8 percent) and February (-1.1 percent). In the first quarter, GDP was 0.3 percent lower than a year ago.

Monthly trend in real gross domestic product

Year-over-year changes in percent

Alfa Bank.ru; Arseniy Anatolyev: The recovery of economic activity exceeded expectations. 04/30/26

According to preliminary calculations by the Ministry of Economic Development, seasonally adjusted real gross domestic product rose by 1.4 percent in March compared to February, following a 0.3 percent increase in February compared to January.

Industrial production in the first quarter was barely higher than in the previous year

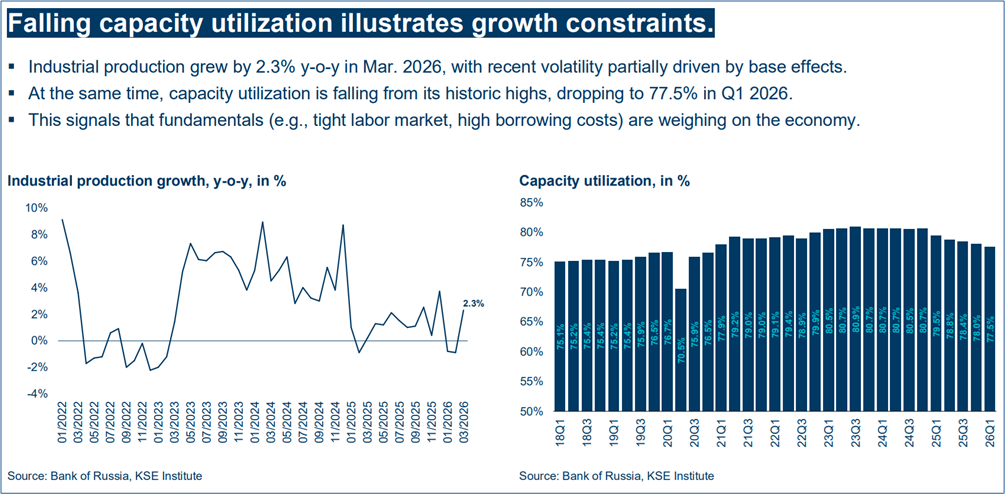

In March 2026, Russia’s industrial production was 2.3 percent higher than a year ago. However, in the first quarter of 2026, it rose by only 0.3 percent year-over-year. In January and February 2026, industrial production actually declined compared to the same months of the previous year.

According to the “Russia Chartbook” published by the Kyiv School of Economics, corporate capacity utilization fell from its historic high reached at the end of 2024 to 77.5 percent by the first quarter of 2026. According to the institute, the causes of the decline include labor shortages and high borrowing costs.

Kyiv School of Economics Institute: Russia Chartbook, April 30, 2026

According to Rosstat estimates, seasonally and calendar-adjusted industrial production rose again by 0.3 percent in March compared to the previous month.

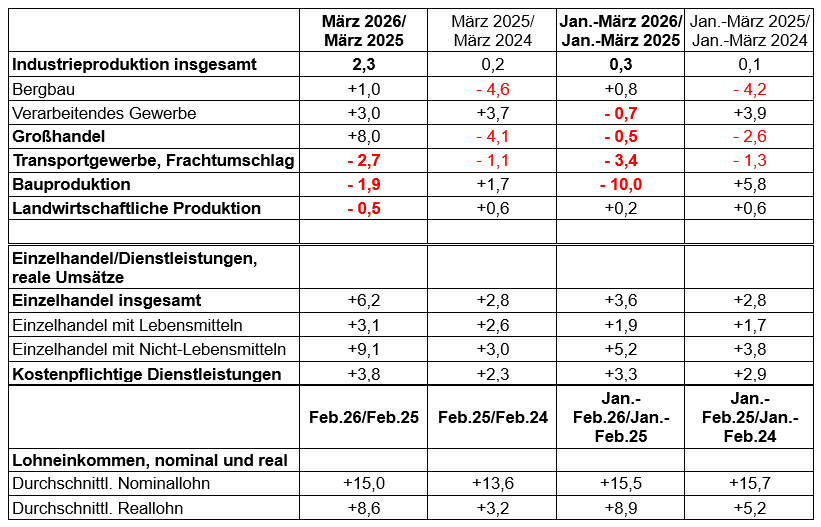

Mining continued to record moderate growth in March 2026 compared to the same month of the previous year (+1.0 percent). The increase in mining production in the first quarter of 2026 was +0.8 percent. Mining was thus a “driver” of the overall weak growth in industrial production of 0.3 percent.

In the “manufacturing sector,” production rose by 3.0 percent year-over-year in March. Production in the “defense-related” industrial sectors continued to grow strongly (“manufacture of other transport equipment,” “pharmaceutical production,” “manufacture of computers, electronic, and optical products”). However, production declined in many “civilian” sectors. In the first quarter of 2026, production in the “manufacturing sector” was still 0.7 percent lower overall than a year ago.

Production in wholesale trade, transportation, and construction declined in the first quarter

Compared to the first quarter of 2025, production also declined in the first quarter of 2026 in wholesale trade (-0.5 percent), transportation (-3.4 percent), and construction (-10.0 percent). Agricultural production in the first quarter of 2026 was only slightly higher than a year ago (+0.2 percent).

Economic Indicators for March 2026 and the First Quarter of 2026

: Year-over-Year Changes in %

Finam.ru; Olga Belenkaya: Slightly negative trend with a recovery in March, Economic conditions in March and the first quarter, April 30, 2026

The consumer sector provided strong growth momentum—amid significantly higher wages

Real retail sales rose by 6.2 percent in March compared to the previous year. According to the Ministry of Economy, the main reason for the increase was growth in sales of passenger cars (+42.1 percent), pharmaceuticals (+14.0 percent), and clothing (+8.8 percent).

In the first quarter of 2026, retail sales rose by a total of 3.6 percent in real terms compared to the previous year. Sales of non-food items grew significantly faster (+5.2 percent) than sales of food items (+1.9 percent).

Real sales in the services sector rose by 3.3 percent in the first quarter, a similar rate of growth to that of retail sales.

Olga Belenkaya notes regarding developments in the retail sector that Rosstat has significantly revised its data upward. She also points out that SberIndex data and current data from the Russian Central Bank on developments in the consumer sector were less positive than the Rosstat data.

Wages continued to rise strongly in January and February. In February, average wages were higher than a year earlier for the second month in a row, by about 15 percent in nominal terms and 8.6 percent in real terms.

Monthly trends in nominal and real

wages: Year-over-year changes in percent

Alfa Bank.ru; Arseniy Anatolyev: The recovery of economic activity exceeded expectations. 04/30/26

According to Belenkaya, however, wage trends varied significantly across industries. Many sectors recorded increases well below the national average.

Recommended reading:

“Die Presse” podcast on the Russian economy:

- Fear in the Kremlin: Are Russians ready to oust Putin from office? Eduard Steiner and Vasily Astrov (wiiw) in conversation with Prof. Gerhard Mangott (University of Innsbruck), April 30, 2026;

- Price shock in oil and gas. Will Europe soon have to buy from Russia again? Eduard Steiner and Vasily Astrov (wiiw) in conversation with international energy consultant Johannes Benigni, April 15, 2026

Spring forecasts from the Vienna Institute for International Economic Studies, wiiw:

Vienna Institute for International Economic Studies; wiiw:

Press release: Andreas Knapp: Spring forecast: Eastern Europe weathering the Iran shock for now, April 29, 2026; Press Releases: English; German

wiiw Forecast Report No. Spring 2026, April 2026: Growth model adapting under pressure; 141 pages; Executive summary by Richard Grieveson, April 29, 2026; wiiw in the press;- bne Intellinews, Clare Nuttall: Impact of Iran-linked shock on Emerging Europe seen as milder than 2022 crisis, says wiiw economist, May 1, 2026, bne Intellinews, Clare Nuttall: Emerging Europe weathers Iran war shock, but risks mount, wiiw says, April 29, 2026

- news ORF.at: Eastern Europe’s economy in upheaval. According to a forecast published Wednesday by the Vienna Institute for International Economic Studies (wiiw), the countries of Central and Eastern Europe (CEE) have so far proven more resilient than the eurozone. 04/29/26

Overall economic development:

- russland.capital: Kremlin acknowledges downward trend in Russia’s economy, May 2, 2026

- The Moscow Times: Russian Growth Outlook Darkens as Ukraine Hits Oil Infrastructure, May 1, 2026

- Globalmsk.ru: The Ministry of Economic Development summarized the economic results for the first quarter of 2026, May 1, 2026

- Alfa Bank.ru; Arseniy Anatolyev: The recovery of economic activity exceeded expectations. Alfa-Bank analysts comment on the latest macroeconomic statistics, April 30, 2026

- Kyiv School of Economics Institute: Russia Chartbook by KSE Institute – Oil Export Revenues Surge due to Iran War; Revenues Set to Improve but Budget Situation Would Only Normalize with Long Conflict, April 30, 2026

- Politkom.ru; Marina Voitenko; Weekly Report: Key Interest Rate Decision in the Context of Risks, 04/30/26

- russland.capital: Nabiullina Rejects Accusations of Hindered Growth; 04/29/26

- Joe Blogs, Video: 50-Day Disaster. For the past 50 days, the price of Brent crude oil has remained above $90 per barrel — and history shows that doesn’t happen very often, April 28, 2026

- Al Jazeera English, Explainer Video: War on Iran: How the Strait of Hormuz crisis boosts Russia’s economic leverage, April 26, 2026

- Finam.ru; Olga Belenkaya: Slightly negative trend with a recovery in March, Economic conditions in March and the first quarter, April 30, 2026; Finam.ru; Olga Belenkaya: The effects of one-off factors on the economy should weaken in the second quarter, April 27, 2026

- RBC.ru: Russia’s GDP fell by 0.3% in the first quarter, April 29, 2026.

- MK.ru; Natalia Trushina: Economist Frumina: “High oil prices do not automatically mean improved welfare for citizens.” MK spoke with Svetlana Frumina, head of the Plekhanov Russian University of Economics, to find out what factors led to Russia’s decline in GDP and how the surge in oil prices due to the Middle East conflict will impact it, April 26, 2026

- BR24, Judith Schacht: Russia’s Economy Under Pressure: Putin Admits Weakness, April 26, 2026

- Fortune, Jason Ma: Russia’s economy minister admits ‘reserves have largely been used up’ while communist lawmaker warns of 1917-style revolution as GDP shrinks, April 25, 2026

- FR.de; Marcus Giebel: Putin Loses Control of Russia’s Economy – Many Sectors in Distress, 04/24/26

- Ntv.de; André Ballin, dpa: Decline instead of growth. Russia’s war economy shrinks unexpectedly sharply, 04/24/26; MSN.com, dpa: Russia faces prolonged economic slump, 04/24/26

- MSN.com; The New Voice of Ukraine: Rising oil prices won’t save Russia’s faltering economy from a recession – Bloomberg, April 22, 2026

- Finam.ru; Alexey Primak, expert at the Institute for Financial and Investment Technologies: Investments are shrinking—and we’re acting as if everything is normal? April 22, 2026

- Kommersant; Artem Chugunov: Industry increased production in March, 04/23/26

- Finmarket.ru: Industrial production in Russia rose by 2.3% in March, April 22, 2026

- The Moscow Times: Russian Companies Freeze Hiring as Demand Cools, Central Bank Says, April 21, 2026

- Finam.ru: Follow-up by Natalia Asedova: Labor Shortages: What Risks Do They Pose to the Russian Economy? 04/21/26

- Merkur.de; Nils Thomas Hinsberger: Putin’s Crisis: Russia’s Economy Still in Danger – Despite Rising Oil Prices, 04/20/26

- ndtv.com; Prateek Shukla: Oil Revenue vs. Ukraine War Bills: Is Russia Hiding Economic Stress? The non-oil deficit remains deeply negative. This means Russia still relies heavily on energy exports to balance its books, April 23, 2026

- The Spectator; Alexander Kolyandr, Centre for European Policy Analysis: Is Russia’s economy really on its last legs? The head of Swedish military intelligence, Thomas Nilsson, told the Financial Times this week that Russia’s economy is far weaker than it appears, and that the Kremlin systematically manipulates its statistics. One need not be a Kremlin agent to find this less than convincing. 04/21/26; inosmi.ru: The Collapse of the Russian Economy: Fact or Fiction? The Spectator: The West is grossly exaggerating Russia’s weakness; Original article; 04/22/26; Euro News; Emma De Ruiter & Dimitri Kavalerov: Russia faked economic data to appear more resilient to its war and sanctions, intel report says, 04/21/26; Business Insider Germany: Russia’s economy is heading toward “a financial catastrophe,” according to Swedish military intelligence, 04/20/26

Fiscal policy; national budget and oil prices:

- bne IntelliNews, Ben Aris: Russia’s economy is cracking — but so is everyone else’s. The war in Ukraine has pushed Moscow’s finances to the brink. A comparison of debt, deficits, and debt-servicing costs reveals that several of Russia’s critics are in comparably troubled fiscal shape, April 27, 2026

- Alfa Bank: The Ministry of Finance will resume foreign exchange transactions in May, April 23, 2026

- Finam.ru: According to Siluanov, inflationary pressures in the Russian economy are stabilizing, 04/18/26

- BondGuide; Alexander Kolyandr and Alexandra Prokopenko (THE BELL): Russia is wasting no time amid high oil prices: but spending is still outpacing revenue, 04/17/26

- Focus.de; Lars-Eric Nievelstein: Russia’s budget deficit blows past the annual target after just three months. Russia’s economy is under pressure. Revenues are weakening significantly, April 17, 2026

- Re:Russia: Oleg Vyugin: Expertise: A Cancelled Manoeuvre: The Challenges Facing Economic and Fiscal Policy in 2026, 04/16/26