Russia: The Growth Surge at Year-End

Author: Klaus Dormann

Throughout 2025, seasonally adjusted production in the Russian economy largely stagnated from month to month through the fall. However, when comparing the production figures for the full year 2025 with those of the previous year, Russia’s real gross domestic product still rose by 1.0 percent, according to the first estimate by the Federal State Statistics Service (Rosstat).

This was due in part to the fact that overall economic output grew noticeably in the last four months of 2025. In December 2025, real GDP reached a new high, according to initial estimates. A chart from the “Institute for Economic Forecasting of the Russian Academy of Sciences” shows that, on a seasonally adjusted basis, it was likely about three percent higher in December than in August.

However, the institute warns against assuming that this growth spurt will continue in 2026. The vast majority of analysts also expect that the increase in aggregate economic output in 2026 will again reach only around one percent. Similarly, the research institute of the state development corporation VEB expects growth of only 0.8 percent. The Russian government, on the other hand, has based its budget planning for 2026 on a slightly higher growth rate of 1.3 percent.

IEF-RAS: Strong GDP Growth Since September

On February 13, the “Institute for Economic Forecasting of the Russian Academy of Sciences” (IEF-RAS) updated its monthly “Short-Term Analysis of Gross Domestic Product Development” based on Rosstat data for December.

Its initial estimate of seasonally adjusted output growth shows a further sharp rise in the real gross domestic product index in December (see the black line in the figure below). The institute estimates seasonally adjusted GDP growth in December at 2.1 percent compared to November.

According to the institute, this sharp increase is likely due, among other things, to “peculiarities in the statistical recording of production output (work volume) by companies operating under government contracts.” This presumably means that services provided by companies under public contracts are allocated by Rosstat to the month of December, even though they were actually provided earlier. Artem Chugunov also reports in Kommersant on several other attempts at explanation.

Estimate of the real gross domestic product

index blue bars: Change in the real gross domestic product index compared to the same month of the previous year, in %

black line: Real gross domestic product index, January 2019 = 100

IEF-RAS: Short-term analysis of GDP dynamics, 02/13/26; data as of 02/10/26

Compared to December 2024, real gross domestic product rose by 1.8 percent according to IEF estimates (see blue bar in the figure above). For the entire fourth quarter of 2025, GDP was 1.3 percent higher than a year ago, according to the Institute’s estimate.

Based on statistical data available in early February, the Institute estimates the GDP growth rate for the full year 2025 at +1.1%, slightly higher than Rosstat’s initial estimate (+1.0%).

The IEF’s “short-term” forecast of 2% for 2026 is likely to be lowered again

In the February edition of its monthly “short-term” forecast, the institute significantly raised its forecast for Russian economic growth in 2026 from 1.3% to 2.0%. However, it explicitly notes:

“It should be particularly emphasized that the upward revision of the growth forecast for 2026 was influenced by the accelerated economic momentum in the fourth quarter and in December 2025. Extrapolating these trends suggests that economic growth could reach around 2% by the end of 2026.

However, there is currently no reason to assume that the factors that accelerated economic activity at the end of 2025 are sustainable. Therefore, once the statistical data for the first quarter of 2026 is available, it is very likely that the forecast for GDP growth in 2026 (+2%) will be revised downward.”

In its latest “Quarterly GDP Forecast” published in mid-December, the Institute expects annual growth in the Russian economy to accelerate to 1.4 percent in 2026 after declining to 0.7 percent in 2025.

IEF: These are the key risks to further growth

According to the IEF, further growth in aggregate economic output in the coming months could be jeopardized primarily by slower growth in consumer demand and a further decline in corporate investment.

The institute also notes that federal budget expenditures fell in January compared to the previous year (-1.4%), while oil and gas revenues in the federal budget were 50.2% lower.

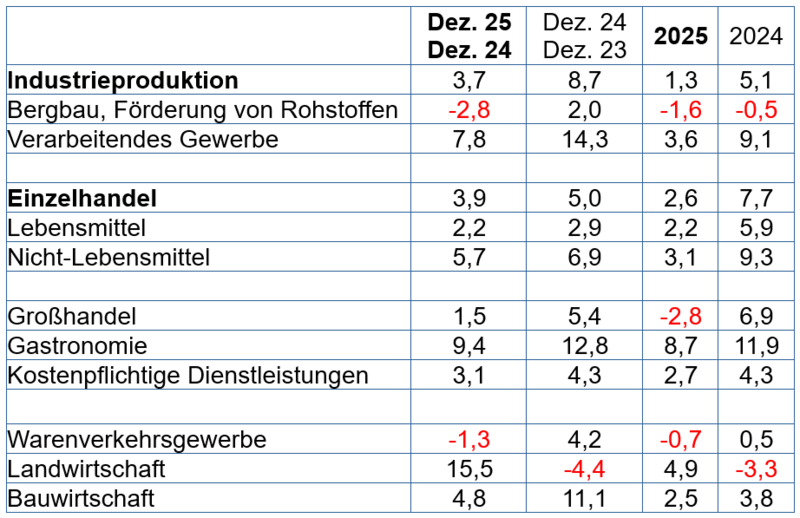

Production Trends in Key Sectors in December 2025

The IEF points out that production in key sectors continued to show very mixed trends in December 2025.

The rise in production accelerated significantly in “manufacturing” (+7.8% compared to December 2024), in construction (+4.8%), and in wholesale trade (+1.5%).

At the same time, other key sectors recorded a decline in production: mining (-2.8%), electricity generation (-1.1%), and freight transport (-1.3%).

Economic indicators for December 2025 and the year 2025

compared with the results of the previous year 2024

Year-over-year changes in %

Sources: Finmarket.ru, 02/06/26; Finam.ru; 02/09/26

Industrial production in 2025: Slower growth in manufacturing, accelerated decline in mining

In the industrial sector, growth in the “manufacturing industry” slowed significantly over the course of 2025. However, following a 9.1 percent increase in 2024, it still achieved a solid growth rate of 3.6 percent. The decline in mining production accelerated from -0.5 percent in 2024 to -1.6 percent in 2025. Overall, industrial production growth fell to 1.3 percent in 2025 (2024: +5.1%).

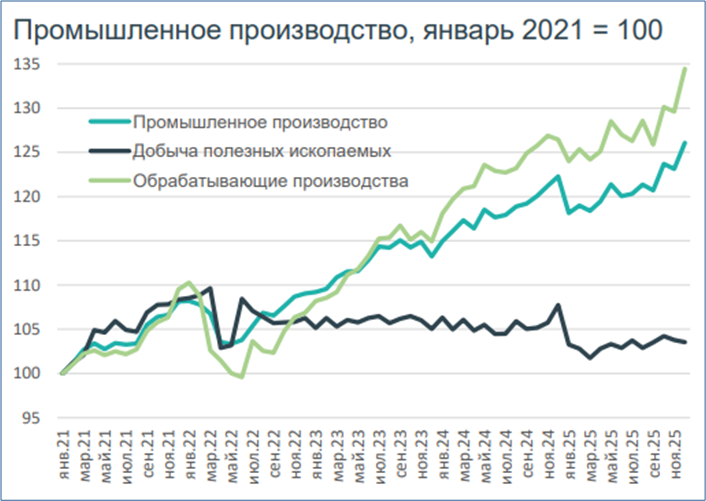

In the following figure, taken from an analysis published on Friday by the research institute of the state development bank VEB.RF, the dark green line shows the seasonally and calendar-adjusted trend of the total industrial production index. It is evident that the “manufacturing sector” has grown at an above-average rate (light green line). In contrast, production in the mining sector declined (black line).

Industrial production (Jan. 2021=100);

seasonally and calendar-adjusted

dark green: total industry; black: mining; light green: manufacturing

VEB Institute: Russia’s Economy in December 2025 – January 2026, Feb. 20, 2026

Defense production drove a sharp rise in industrial output

The IEF cites the following three sectors, which primarily contribute to the production of defense products, as the main drivers of strong growth in the manufacturing sector in December 2025 (+7.8%): The production of other transport vehicles and equipment (+28.6% compared to Dec. 2024); the manufacture of metal products (+21.5%); and metal extraction, so-called “metallurgy” (+16.9%).

The production of pharmaceuticals rose by 12.9% compared to December 2024.

At the same time, 14 economic sectors—which, at 48 percent, accounted for nearly half of total manufacturing output—recorded a decline in production.

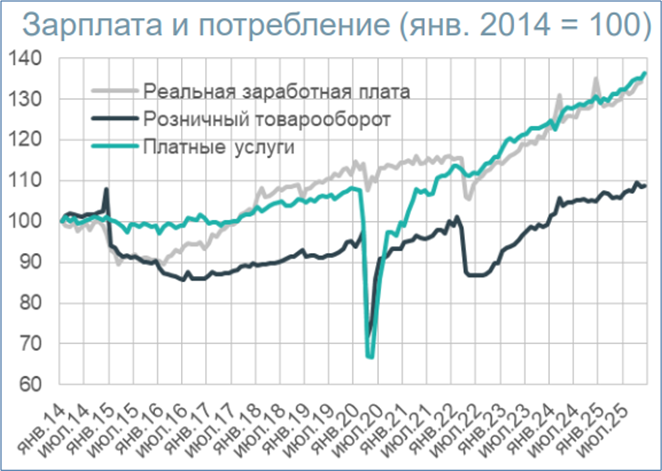

The growth driver “private consumption” also lost momentum in 2025

In the retail sector, the service sector, and the hospitality industry, real sales in 2025 also grew significantly more slowly than in 2024. Nevertheless, according to the IEF, consumer demand remained the most important “engine of the economy.” Real retail sales rose by 3.9% in December 2025 compared to the same month the previous year. Sales in the hospitality sector continued to grow at an even stronger rate (+9.4%). In the paid services sector, sales were 3.1% higher in December (Finmarket).

Real wages and consumption (Jan. 2014 = 100);

seasonally and calendar-adjusted

gray line: real wages; black line: real retail sales;

green line: real sales of fee-based services

VEB Institute: Global Economy and Markets, 02/13/26

Real disposable income grew by 7.4 percent in 2025

Consumption growth was supported by a significant increase in real wages (+4.8% from January to November 2025 year-over-year; Finam.ru). The rise in wages contributed significantly to the continued very strong growth in real disposable income, which Rosstat estimates at 7.4 percent in 2025 (Interfax).

Index of real disposable income,

seasonally and calendar-adjusted (Q4 2013=100)

VEB Institute: Global Economy and Markets, February 13, 2026

Despite the strong rise in incomes, growth in private consumption slowed significantly in 2025 compared to 2024. According to estimates by the Ministry of Economy, private consumption rose by only 2.9% in 2025. In 2024, however, it had grown by 7.1% (Kommersant).

The VEB Institute forecasts GDP growth of just 0.8% for 2026

The chief economist of the VEB Institute, former Deputy Minister of Economic Development Andrey Klepach, recently presented new economic forecasts from the VEB Institute at an economic conference in Sochi ("Mountain Grain Assembly 2026") (oilworld.ru reported). On Friday, the VEB Institute also published the forecasts in its report “Russia’s Economy in December 2025 – January 2026.” In summary, Klepach and the VEB Institute expect the following trends for the Russian economy:

GDP growth will be slightly weaker in 2026, but industrial output will grow more strongly than in 2025

Annual growth for the overall economy will slow from around 1 percent in 2025 to 0.8 percent in 2026. However, industrial production growth—which slowed sharply in 2025—will accelerate from 1.3 percent to 2.4 percent.

The VAT increase, the continued restrictive monetary policy, and the expected decline in investment in the energy sector will negatively impact economic growth in early 2026. In the “medium term,” in 2027 and 2028, GDP growth is expected to pick up to around 2.5 percent.

Preliminary economic data and forecasts from the VEB Institute

| Indicators, % year-on-year | Nov. 25 | Dec. 25 | Q4 25 | Q1 26 | 2024 | 2025 | 2026 |

| Forecast | Forecast | ||||||

| Gross Domestic Product, GDP | 0.3 | 1.7 | 1.1 | 1.0 | 4.9 | 1.0 | 0.8 |

| Total industrial production | 0.4 | 3.7 | 2.3 | 4.1 | 5.1 | 1.3 | 2.4 |

| Manufacturing | 1.0 | 7.8 | 4.3 | 5.4 | 9.1 | 3.6 | 3.5 |

| Retail, real sales | 3.3 | 3.9 | 4.0 | 1.2 | 7.7 | 2.6 | 1.7 |

| Services, real revenue | 3.4 | 3.1 | 3.3 | 3.4 | 4.3 | 2.7 | 1.8 |

| Real wages | 5.8 | – | 4.3* | 5.1 | 9.7 | 4.4* | 3.7 |

| Real disposable income | – | – | 5.8 | 6.1 | 8.2 | 7.4 | 1.0 |

| Investments in property, plant, and equipment | – | – | -1.2* | -6.1 | 7.4 | 0.4* | -0.9 |

*) Forecasts by the VEB Institute

VEB Institute: Russia’s Economy in December 2025 – January 2026, Feb. 20, 2026

Incomes are rising much more slowly, and consumer demand is waning

Growth in real disposable income will slow sharply in 2026 due to the increase in the value-added tax and lower corporate earnings. It will no longer reach 7.4 percent as in 2025, but only 1.0 percent. Real wage growth will slow from 4.4 percent to 3.7 percent in 2026.

Consumer demand is expected to decline at the start of 2026. In 2026, real retail sales growth will slow to 1.7 percent (2025: +2.6%). Real sales in the services sector will grow by only 1.8 percent in 2026 (2025: +2.7%)

Fixed investment will decline by 0.9 percent in 2026 compared to 2025

Growth in investment in tangible assets is expected to have fallen to just 0.4 percent by 2025. In 2026, a decline in fixed investment of 0.9 percent is expected due to restrictive monetary policy and a higher tax burden.

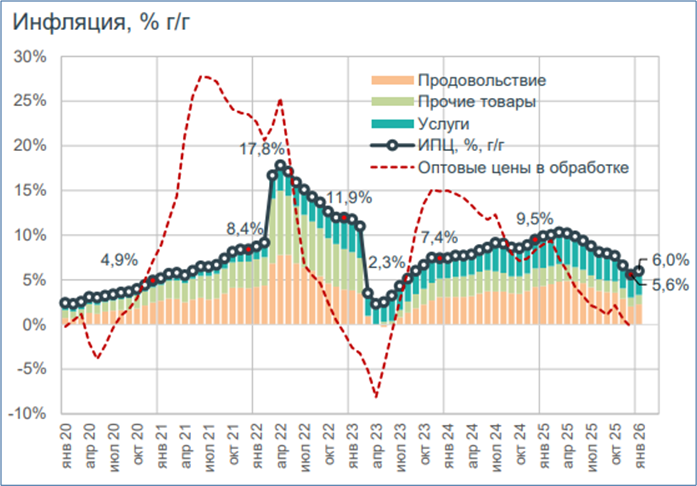

Inflation will be slightly higher at the end of 2026 than at the end of 2025

In December 2025, the annual increase in consumer prices fell to just 5.6%, as shown by the black line in the following figure. In January, the inflation rate rose to 6.0% with the increase in the value-added tax. The colored bar segments show the contribution of food, non-food items, and services to the overall increase in consumer prices. The red line shows the rate of change in industrial producer prices.

Year-over-year increase in consumer prices in percent

VEB Institute: Russia’s Economy in December 2025 – January 2026, February 20, 2026

In December 2026, the annual increase in consumer prices will be slightly higher than at the end of 2025, at 6.2%, according to the VEB Institute. By the end of 2027, it is expected to still significantly exceed the central bank’s inflation target of 4%, at 5.3%.

The key interest rate, which was lowered to 16% in December 2025, will fall to 12% by the end of 2026 and to 7% by the end of 2027.

The budget deficit and public debt are rising significantly

In 2026, total government revenues will rise slightly, although revenues from the oil and gas sector will continue to decline. With spending growing further to 45.9 to 47.8 trillion rubles in 2026, the budget deficit will rise to 3.8 to 5.8 trillion rubles in 2026.

Significant borrowing will be required as early as the first quarter of 2026. Public debt will rise significantly from 31.2 trillion RUB (14.6% of GDP) in 2025 to 39.5 to 41.0 trillion RUB (17.6–18.1% of GDP) in 2026.

Declining energy exports may recover moderately in 2026

In 2025, exports from the fuel and energy sector declined due to sanctions and increased competition. With a refocus on Asian and African markets, moderate growth is expected for the second half of 2026. Increased natural gas deliveries to China via the Power of Siberia pipeline will support exports. There is a risk of stagnation in LNG exports due to sanctions.

The price of Russian Urals crude fell to an average of $55.6 in 2025 (in December: $39). A further decline to $48 to $51 is expected as the annual average for 2026 (with a Brent price of around $65).

Recommended reading:

- German-Russian Chamber of Foreign Trade:

Focus Analyses, German; also Russian; (selection): Weak growth, declining available reserves, and high military spending, 02/18/26 - Podcast “Tsars, Data, Facts” by the German-Russian Chamber of Foreign Trade, hosted by Thomas Baier: From Boom to Stagnation: Russia’s Economy in 2026; Guest: Vasily Astrov, 36 min., Feb. 17, 2026

- DW.com.ru; Stuart Brown: LNG Imports: Is Europe Falling into a New Dependence on the U.S.? The U.S. has replaced Russia as Europe’s leading gas supplier; 02/21/26

- Joe Blogs video: Russia hits new lows. Russia’s oil and gas revenues have plunged to their lowest level since 2020. But the bigger story may be price. 02/19/26

- VEB Institute: Russia’s Economy in December 2025 – January 2026, with Forecasts for 2026. 02/20/26

- Politcom.ru; Marina Voitenko: The Central Bank warned of inflation risks, 02/19/26

- The Bell; Denis Kasyanchuk: GDP Data – What They Reveal, What They Hide, 02/18/26; The Bell; Denis Kasyanchuk: The Bell’s Monthly Briefing — January, 02/12/26

- Joe Blogs video: Russian Food Crisis. Food prices in Russia are back in focus — and this time it’s cucumbers leading the headlines. Official data shows food inflation running at 5.88% in January, just below the overall inflation rate of 6%, 02/18/26

- Focus.de; Jennifer Braunstein: Looming Economic Crisis. War in Ukraine Drives Up Prices: Life in Russia Is Becoming Increasingly Expensive; 02/19/26; BBC.com; Olga Shamina, Yaroslava Kiryukhina, Sergei Kagermazov: Food prices are surging in Russia. Is the war hitting Russians in the pocket? 02/18/26

- AOL; Reuters; Andrew Osborn: In Russia, the humble cucumber becomes the latest symbol of rising wartime prices, 02/17/26

- Finmarket.ru: Inflation in Russia stood at 1.62%in January. The annual inflation rate accelerated from 5.59% in the previous month to 6.00%, 02/13/26

- Institute for Economic Forecasting of the Russian Academy of Sciences; IEF-RAS: Short-term analysis of GDP dynamics, 02/13/26

- Kommersant; Artem Chugunov: The sustainability of GDP growth will be tested, 02/18/26; Household demand remains high. Alfa Bank’s estimate of consumption in January, 02/16/26; Companies have offered varying assessments of the business climate, 02/12/26; December saves the year. The last month of 2025 gave the economy a boost, 02/11/26

- Phoenix Roundtable: The Putin System – How Strong Is Russia? Anke Plättner discusses with: Katja Gloger, journalist; Michael Thumann, Moscow correspondent, Die Zeit; Roman Goncharenko, Deutsche Welle; Prof. Alexander Libman, Institute for Eastern European Studies, Freie Universität Berlin, February 18, 2026

- Focus online; Anna Schmid: An old joke is circulating in Russia due to Putin’s economic slump. Oil revenues are falling, the government deficit is growing. Political scientist Alexander Libman explains in a recent interview what an old joke has to do with the situation, 02/18/26

- Ukrinform; english.nv.ua; Alona Sonko: Russia’s economy is fragile but not facing imminent collapse – expert, summary of the following Ukrinform interview with Mykhailo Honchar, 02/18/26; ukrinform.ua; Myroslav Liskovich, Kyiv: Mykhailo Honchar, President of the Center for Global Studies “Strategy XXI”: Russia acts according to the logic of a crocodile, which is destroyed not so much by force as by cunning, 02/17/26

- Nezavisimaya Gazeta; Anastasia Bashkatova: The transition to a high-wage economy is being delayed, 02/17/26

- Finam.ru; Olga Belenkaya: Inflation in Russia was below expectations in January, 02/16/26

- Alfa Bank: The Central Bank surprised with a cautious signal. What will the next decision look like? The chances of continued key rate cuts; 02/16/26

- Gaidar Institute Commentary: Yevgeny Goryunov: “The Central Bank’s decision to cut the key rate was unexpected, but justified by the dynamics of core inflation.” 02/15/26

- Joe Blogs Video: Russia’s central bank has just made a shock move — cutting interest rates to 15.5% at a time when inflation is rising again. • Inflation is rising again • VAT has just been raised from 20% to 22% • Inflation expectations have climbed to 13.7% • The ruble has been strengthening • Corporate profits are under pressure • GDP growth is slowing So why cut rates now? 02/15/26

- Finmarket.ru: Inflation in Russia stood at 1.62%in January. The annual inflation rate accelerated from 5.59% in the previous month to 6.00%, 02/13/26