Russian business leaders: Key interest rates need to be cut further

Author: Klaus Dormann

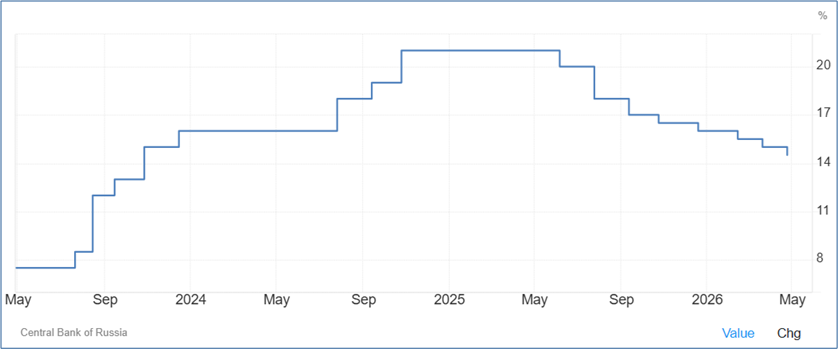

On April 24, the Russian Central Bank lowered its key interest rate again, this time by only half a percentage point, to 14.5 percent per year. The Russian Union of Industrialists and Entrepreneurs had previously called for a cut twice as large—one percentage point—to boost growth.

According to estimates by the Ministry of Economy, total economic output in the first two months of 2026 was 1.8 percent lower than a year ago. However, in its medium-term economic forecast updated in conjunction with the key interest rate decision, the Central Bank maintains that the Russian economy is expected to grow by 0.5 to 1.5 percent year-over-year in 2026 as a whole. Almost all forecasts from international economic organizations, research institutes, and banks currently fall within this range.

As reported by Handelsblatt, the Vienna Institute for International Economic Studies (wiiw) also expects Russia’s economic growth to remain at around one percent in its spring forecast, which will be officially presented at the end of April. Previously, the institute had assumed that Russia’s economic growth would accelerate from 1.0 to 1.2 percent this year. Now, according to Handelsblatt, it is slightly lowering its growth forecast for 2026 to 0.9 percent. According to the article, wiiw’s Russia expert, Vasily Astrov, expects higher revenues from oil sales to have a “major one-off effect” on the Russian state budget. However, the government will primarily use the additional revenue to reduce the budget deficit, not for “economic stimulus programs” (FR.de).

The key interest rate has been cut by a total of 6.5 percentage points since June 2025

To curb inflation, the central bank had raised the key interest rate in October 2024 to a long-standing record high of 21 percent. It did not begin lowering the high key interest rate until early June 2025. It most recently continued the “easing” of its monetary policy—which had been widely criticized as too “restrictive”—in February and March with two further small steps, each involving a 0.5 percentage point cut in the key interest rate (Interfax.com).

Russian Central Bank Key Interest Rate in Percent per Year

Trading Economics: Russia Interest Rate

The Central Bank raised its key interest rate forecast slightly due to higher inflation risks

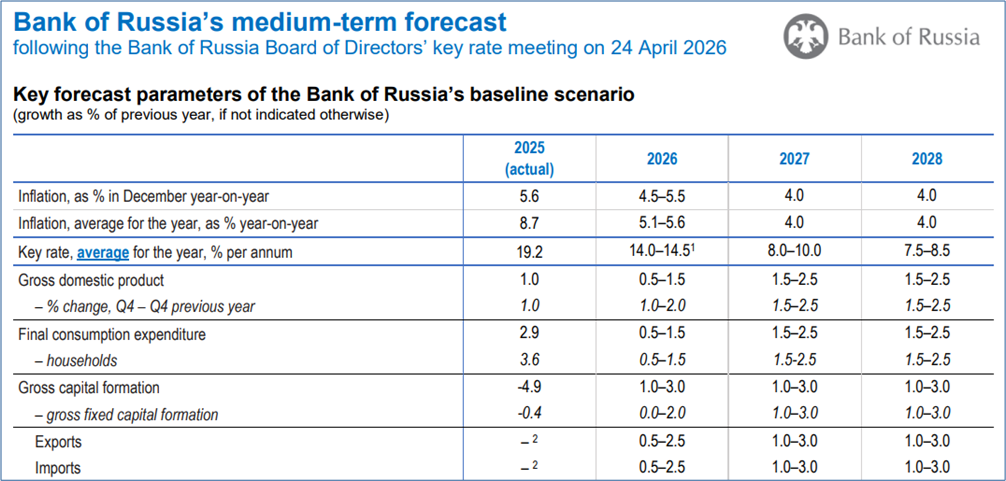

The central bank’s baseline forecast assumes that the key interest rate will average 14.0 to 14.5% in 2026, about 5 percentage points lower than in 2025. In 2027, with an inflation rate of 4 percent, the key interest rate is expected to be further lowered to 8.0 to 10.0% per year (see the third row of the table below).

In her statement on the key interest rate decision, Central Bank President Nabiullina noted that the Central Bank has thus raised its key interest rate forecast slightly. The reason for this is that inflation risks in Russia have increased significantly due to the conflict in the Middle East and also in light of developments in the state budget.

The annual inflation rate is expected to fall from 8.7% to 5.1–5.6% in 2026

According to the central bank’s forecast, the annual increase in consumer prices will fall to 4.5 to 5.5% in December 2026 (see first row of the table).

On average for 2026, the central bank expects an inflation rate of 5.1 to 5.6%. In 2025, it had been 8.7%. Starting in 2027, the forecast indicates that the rate of price increase will align with the Central Bank’s inflation target of 4.0%.

Russian Central Bank:

Forecasts for Inflation, Key Interest Rate, and Growth

Year-over-year growth in %, unless otherwise stated

Bank of Russia: Bank of Russia’s medium-term forecast, April 24, 2026; excerpt

The Central Bank continues to expect economic growth of 0.5 to 1.5% in 2026

The Central Bank’s press release on the key interest rate decision notes that Russia’s economic growth “according to high-frequency data” slowed in the first quarter of 2026. However, the Central Bank does not provide its own estimate for the growth rate in the first quarter.

Among other factors, the Central Bank cites the economy’s reaction to tax changes as a cause of the slower growth in the first quarter (presumably referring to business activities brought forward to 2025 due to the value-added tax increase scheduled for early 2026). Other factors that put the brakes on growth in the first quarter included the lower number of working days and unfavorable weather conditions. Because the slower growth in the first quarter of 2026 was thus significantly influenced by “one-time factors,” the central bank is sticking to its previous forecast for growth in 2026 as a whole of 0.5 to 1.5%.

"Precise" details on 2026 growth can only be provided after two quarters

Central Bank President Nabiullina noted in her statement that the first two months of 2026 had three fewer working days than January and February 2025. According to the Central Bank’s estimates, this led to a decline in annual GDP growth of up to 0.5 percentage points in the first quarter of 2026. In the second quarter, however, the months of May and June would have three more working days than in the previous year. Nabiullina draws the following conclusion:

“All of this means that we will only be able to assess the development of production more accurately once we look at the statistics for the first six months of 2026 as a whole.”

Regarding Russia’s growth outlook, the Central Bank President currently states:

“According to our estimates, the moderate economic performance in the first quarter of 2026 will be offset in subsequent periods. In addition to calendar effects, this will be driven by a partial recovery in consumer spending and investment activity, which is already evident in the high-frequency data for March and April.

Higher prices on global commodity markets are likely to provide additional support for domestic demand. Against this backdrop, we confirm our GDP growth forecast for this year unchanged at 0.5 to 1.5%.”

Nabiullina reiterated at the press conference that she sees no risk of the economy “overcooling.” She emphasized that the central bank would only lower interest rates more quickly if inflation fell from its current level of 5.9% below the 4% target and unemployment began to rise. Nabiullina’s first deputy, Alexei Zabotkin, stated that the first-quarter GDP data, to be released in May, would differ “for the better” from the data for January and February (Reuters).

What signs point to a revival in growth

Nabiullina points to signs that Russian companies are ramping up their investment plans and that consumer demand could pick up. Given the rise in energy and commodity prices on global markets, companies in the mining sector may now be revising their investment plans upward. Construction companies are now trying to make up for weather-related production losses from the winter.

According to Nabiullina, there were also signs of a recovery in consumer demand in March, particularly in car sales. Overall, however, consumption growth in 2026 will be more moderate than in 2025. In its medium-term forecast, the Central Bank expects growth in household consumption to slow from 3.6% in 2025 to just 0.5 to 1.5% in 2026. For gross investment, it expects growth of 1.0 to 3.0%, following a 4.9% decline last year (see table above).

The labor market situation is gradually easing

In its press release, the central bank notes that unemployment remains at a historic low and that wages continue to rise faster than labor productivity. At the same time, however, it notes that, according to surveys, the proportion of companies reporting labor shortages continues to decline. It is now at its lowest level since mid-2023. Companies are now planning more moderate wage adjustments for 2026 than in the 2023–2025 period.

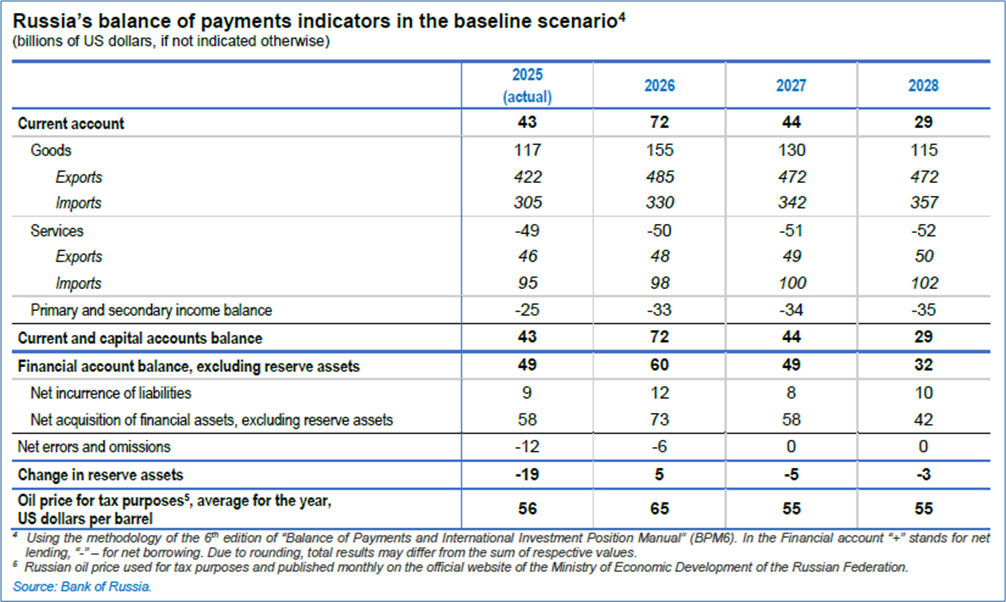

The oil price forecast was raised by $20 to $65 per barrel

Regarding Russia’s external economic development in light of the war in the Middle East, Nabiullina said:

“The situation in the Middle East remains uncertain. According to our baseline scenario, the conflict will result in a slowdown in global economic growth, a worldwide increase in logistics and energy costs, higher global inflation, and higher interest rates.”

In its forecasts for Russia’s external economic development, the Central Bank made the following changes, among others, compared to the forecast from February 13:

The forecast for the Russian oil price (for tax purposes) in 2026 was raised from $45 to $65 per barrel (see the last row of the table below).

Russia’s revenue from goods exports will rise by about 15% in 2026, from $422 billion to $485 billion. In February, exports were still expected to decline to $399 billion.

The trade surplus is now projected to be $155 billion in 2026, about 70% higher than previously estimated ($90 billion).

However, according to the Central Bank’s assessment, the impact of these additional export revenues on the ruble exchange rate will be largely offset by government intervention in the foreign exchange market and the application of so-called “fiscal rules.”

Russian Central Bank:

Development of the balance of payments and oil price through 2028

(in billions of U.S. dollars, unless otherwise noted)

Bank of Russia: Bank of Russia’s medium-term forecast, April 24, 2026; excerpt

Risks to the Central Bank’s Forecasts

Central Bank Governor Nabiullina also sees risks for Russia stemming from the war in the Middle East. She emphasized:

“If the conflict drags on, the negative impact on the Russian economy will intensify. The consequences of rising global costs could prove more severe than the benefits of higher exports and a stronger ruble.”

At the same time, Nabiullina also drew attention to inflation risks that could stem from developments in the Russian federal budget. In the first quarter of 2026, government spending had significantly exceeded the already high levels of the previous year. The president emphasized that the central bank must curb lending all the more as the “fiscal stimulus” for demand increases. This means that the higher the budget deficit, the higher the key interest rate must be kept.

RSPP Business Association Had Called for a One-Percentage-Point Cut

Alexander Schochin, chairman of the Russian Union of Industrialists and Entrepreneurs (RSPP), had urged the Central Bank’s Board of Directors prior to the key interest rate decision to cut the key interest rate by a full percentage point. If the key interest rate were to fall from 15 to 13 percent by the end of the year through gradual cuts of only half a percentage point each time, this would not be enough to stimulate investment. “It would be right to take more radical measures here and lower the interest rate by one percentage point, rather than taking small steps of 0.5 percentage points,” Interfax quoted Shokhin as saying (Kommersant.ru).

Schochin commented on the decision to lower the key interest rate to 14.5% on the radio station Business FM as follows (RSPP press release):

“When I called for a 1% interest rate cut, I meant that we could reach 10% or perhaps even a single-digit figure by the end of the year.” Such rates are crucial for fostering investment willingness not only for large companies but also for small and medium-sized enterprises.

“Many investment projects are currently on hold,” explained the chairman of the Russian Union of Industrialists and Entrepreneurs. “A recovery in investment activity is possible at a rate below 10%. The Central Bank traditionally calls for a focus on inflation trends. This requires not only scientific insights—models, formulas, etc.—but also a delicate touch. We need a sense of how, on the one hand, to prevent production from falling below the level of a cooling economy, and on the other hand, not to fuel the inflationary spiral.”

Vice President Alexander Murychev stated in an RSPP press release that the key interest rate cut is, of course, a positive signal. However, the magnitude of the cut is not sufficient to meet companies’ need for significantly cheaper loans.

Fundamental criticism of the central bank’s monetary policy and the government’s economic policy from Russian business circles is documented in a two-part report by russland.capital (with video interviews) on the “Moscow Economic Forum,” in which Sergei Glazyev, State Secretary of the Union State of Russia and Belarus, also participated.

Will Elvira Nabiullina be replaced as president of the Russian Central Bank?

In the run-up to the key interest rate decision, Mike Eckel explored in an article for “Radio Free Europe Radio Liberty” whether Elvira Nabiullina, who has headed the Central Bank for nearly 13 years, has now also fallen out of favor with President Putin.

Dismissing Nabiullina now would sever the only “institutional anchor” that has maintained the “credibility of the markets,” Aleksandra Prokopenko, a former advisor to the Central Bank and current employee of the Carnegie Russia Eurasia Center in Berlin, told him. For Prokopenko, Nabiullina’s replacement would be a sign of the government’s weakness. By law, her term as Central Bank president ends in a year. Prokopenko said it is unlikely that Putin will replace her before then. For Prokopenko, the “more interesting question” is whether an independent figure at the helm of the Central Bank will be less or more welcome to the Kremlin a year from now, given the political conditions.

“If they fire Nabiullina, the entire economy will panic,” said Nicholas Birman-Trickett (S&P Global Associate Director). In his view, “the Kremlin” does want lower interest rates. But President Putin also knows that a “yes-man” at the helm of the Central Bank would be disastrous.

Richard Portes, a professor at London Business School, told Eckel: “There is no one better qualified to lead the Russian Central Bank than Nabiullina.” “Putin can rant all he wants. That won’t improve the state of the Russian economy, which is pretty disastrous,” said Portes. “I think he has every reason to be concerned.”

What Eckel reports on growth and public finances

Mike Eckel summarized the economic development of the Russian economy in his article as follows: Last year, GDP growth slowed significantly: from 4.9 percent in 2024 to just 1 percent in 2025. In the first two months of 2026, the economy contracted by 1.8 percent year-over-year, according to government estimates. The government signaled that its current growth forecast for 2026 of 1.3 percent may soon be revised downward.

The economic turnaround was reflected in the federal budget: The deficit skyrocketed to 4.5 trillion rubles ($60 billion) in the first three months of 2026. It is roughly twice as high as in the same period last year, because revenue from oil exports declined (Eckel refers to preliminary estimates from the Ministry of Finance dated April 8).

Reshetnikov: The economy’s reserves are “largely exhausted”

Eckel also quotes from a speech by Economy Minister Maxim Reshetnikov at an economic forum in Vladivostok, citing a report in the daily newspaper Nezavisimaya Gazeta. According to an Interfax report, the economy minister argued at the economic forum, among other things, that:

The situation of the Russian economy is currently more difficult than in recent years due to the strong ruble, high interest rates, labor shortages, and limited public spending capacity. Until now, there were still some reserves in the economy. However, these reserves are now largely depleted. The macroeconomic situation has become significantly more difficult.

The ruble exchange rate is currently stronger than we would like—and is likely to remain so in the future—and is stronger than we had assumed in earlier forecasts.

Interest rates are also quite high. Of course, it is encouraging that they are falling, but given the current budget situation and other factors, interest rates are likely to decline somewhat more slowly than we would like.

The main task for companies in the near future is therefore to cut costs, find ways to make optimal use of available resources, and ultimately increase labor productivity. The government’s role is to support them in this effort.

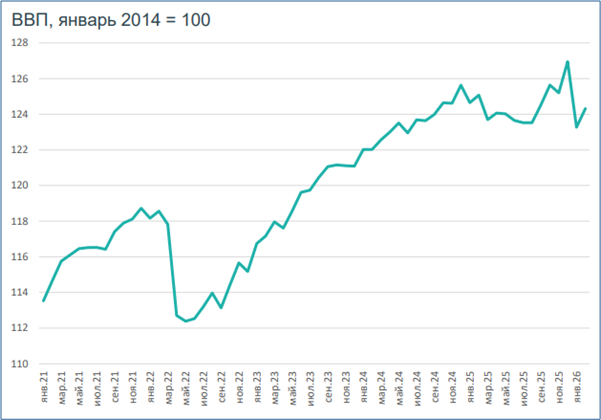

VEB Institute estimates on GDP growth in the first two months

The VEB Institute has published estimates of how the Russian economy’s output has developed through February 2026, seasonally and calendar-adjusted. According to these estimates, following a sharp decline in January, Russia’s gross domestic product rose by 0.8% in February compared to the previous month.

Real Gross Domestic Product Index;

seasonally and calendar-adjusted; Jan. 2014=100

VEB Institute: Russia’s Economy in February/March 2026, April 10, 2026

Construction, wholesale trade, freight transport, services, and industrial production contributed to the rise in real gross domestic product in February. Passenger transport and the restaurant industry, on the other hand, recorded a decline in output. Agriculture and retail trade showed virtually no growth.

Recommended reading:

Monetary Policy:

- Russian Union of Industrialists and Entrepreneurs: Alexander Shokhin assessed the possibility of the key rate reaching single digits, April 24, 2026; Commentary by RSPP Vice President Alexander Murychev on the Central Bank’s key rate decision; April 24, 2026

- Finam.ru; Olga Belenkaya: The Russian Central Bank expects a key rate cut and a slightly upwardly revised forecast, 04/24/26; Finam.ru; Olga Belenkaya: The key rate was cut as expected, and the forecast was revised downward, April 24, 2026

- The Moscow Times: Russia’s Central Bank Cuts Key Rate to 14.5%, April 24, 2026

- Interfax.com: The Russian Central Bank cuts the key rate by 50 basis points to 14.5% per year, April 24, 2026; Interfax.com: Central Bank maintains forecast for Russia’s GDP growth in 2026 at 0.5%–1.5%, and at 1.5%–2.5% for 2027, April 24, 2026; Interfax.com: Investment in Russia will return to the previous year’s level in 2026; March and April point to a recovery, according to the Central Bank governor, April 24, 2026; Interfax.com: The rise in inflationary risks requires a more cautious approach to monetary policy decisions – Governor of the Central Bank of Russia, April 24, 2026

- RTE 100; AFP: Russia cuts benchmark interest rate to 14.5% as economy slows, April 24, 2026

- Reuters; Published by Global Banking & Finance Review®: Russian Central Bank Cuts Key Rate by Only 50 Bps, Raises Oil Price Forecast on Iran War, April 24, 2026

- Bank of Russia: Statement by Bank of Russia Governor Elvira Nabiullina following the Board of Directors meeting on April 24, 2026, April 24, 2026

- Bank of Russia; Press Release: Bank of Russia cuts the key rate by 50 basis points to 14.50% p.a., April 24, 2026

- Briefly News.com; Bloomberg: Russia’s central bank is likely to cut interest rates again as the economy loses momentum, April 24, 2026

- Kommersant: The Chairman of the Russian Union of Industrialists and Entrepreneurs (RSPP) called on the Central Bank of Russia to cut the key rate by one percentage point, 04/23/26

- Reuters; published by Global Banking & Finance Review®: Russia’s Economic Contraction May Spur Key Rate Cuts, Analysts Say, April 23, 2026

- Kommersant: Reshetnikov: The task of reducing inflation in Russia has largely been accomplished, April 23, 2026

- FOCUS Online Editorial Team: Billions in losses. Putin acknowledges economic problems – Russian banks are sitting on loans, 04/22/26; Yahoo Finance; The Telegraph, Melissa Lawford: A banking crisis made in the Kremlin is gripping Russia, 04/22/26

- Radio Free Europe, Radio Liberty; Mike Eckel: Entangled In Russia’s Faltering Economy: The Fate Of Its Respected Central Banker, April 21, 2026

- Ostwirtschaft.de: Russia’s fight against inflation is getting tougher. High wages, robust demand, and new external economic risks are complicating Russia’s fight against inflation, April 21, 2026

Fiscal Policy; National Budget and Oil Prices:

- Finam.ru: According to Siluanov, inflationary trends in the Russian economy are stabilizing, April 18, 2026

- Re:Russia: Oleg Vyugin: Expertise: A Cancelled Manoeuvre: The Challenges Facing Economic and Fiscal Policy in 2026, April 16, 2026

- BondGuide; Alexander Kolyandr and Alexandra Prokopenko (THE BELL): Russia is wasting no time with high oil prices: but spending is still outpacing revenue, 04/17/26

- Focus.de; Lars-Eric Nievelstein: Russia’s budget deficit blows past the annual target after just three months. Russia’s economy is under pressure. Revenues are weakening significantly, April 17, 2026

Overall economic development:

- FR.de; Marcus Giebel: Putin is losing control of Russia’s economy – many sectors in distress, 04/24/26

- Ntv.de; André Ballin, dpa: Decline instead of growth. Russia’s war economy is shrinking unexpectedly sharply, 04/24/26; MSN.com, dpa: Russia faces a prolonged economic slump, 04/24/26

- MSN.com; The New Voice of Ukraine: Rising oil prices won’t save Russia’s faltering economy from a recession – Bloomberg, April 22, 2026

- Finam.ru; Alexey Primak, expert at the Institute for Financial and Investment Technologies: Investments are shrinking—and we’re acting as if everything is normal? April 22, 2026

- The Moscow Times: Russian Companies Freeze Hiring as Demand Cools, Central Bank Says, April 21, 2026

- Finam.ru: Follow-up by Natalia Asedova: Labor Shortage: What Risks Does It Pose to the Russian Economy? 04/21/26

- Merkur.de; Nils Thomas Hinsberger: Putin’s Crisis: Russia’s Economy Still in Danger – Despite Rising Oil Prices, 04/20/26

- ndtv.com; Prateek Shukla: Oil Revenue vs. Ukraine War Bills: Is Russia Hiding Economic Stress? The non-oil deficit remains deeply negative. This means Russia still relies heavily on energy exports to balance its books, April 23, 2026

- The Spectator; Alexander Kolyandr, Centre for European Policy Analysis: Is Russia’s economy really on its last legs? The head of Swedish military intelligence, Thomas Nilsson, told the Financial Times this week that Russia’s economy is far weaker than it appears, and that the Kremlin systematically manipulates its statistics. One need not be a Kremlin agent to find this less than convincing. 04/21/26; inosmi.ru: The Collapse of the Russian Economy: Fact or Fiction? The Spectator: The West is grossly exaggerating Russia’s weakness; Original article; 04/22/26; Euro News; Emma De Ruiter & Dimitri Kavalerov: Russia faked economic data to appear more resilient to its war and sanctions, intel report says, 04/21/26; Business Insider Germany: Russia’s economy is heading toward “a financial catastrophe,” according to Swedish military intelligence, April 20, 2026

- Nezavisimaya Gazeta; Anastasia Bashkatova: The budget cannot subsidize loans for everyone who wants them. Minister of Economic Development Maxim Reshetnikov stated that the economy’s reserves are depleted, April 19, 2026; Interfax.com: The Russian economy’s reserves are largely depleted, and the macroeconomic situation is more difficult than in recent years – Reshetnikov, April 17, 2026

- LIGA.net news editor Vira Kasiyan: Russia admits that the economy’s reserves are “nearly exhausted.” The Minister of Economic Development of the Russian Federation stated that the macroeconomic situation is significantly more difficult than in previous years, 04/17/26

- Jungle World; Katja Woronina: Putin is calling for a pay-up. Russia’s economy is under pressure. Private debt is rising, the economy is weakening, and the budget deficit is growing, 04/16/26

War, Energy Supply, Energy Prices, and Russia:

- Dow Jones; Dr. Dafne Ter-Sakarian, Senior Analyst, Russia & Eurasia: Moscow will use Iran war windfall to avoid budget cuts, April 22, 2026

- DW.com. Arthur Sullivan: Russia to block Kazakh oil flows to Germany via key pipeline, April 22, 2026

- tagesschau.de: Crude oil from Kazakhstan. Russia halts oil transit to Germany, 04/22/26

- Berliner Zeitung, Flynn Jacobs: Druzhba Pipeline. Russia halts Druzhba oil: Gasoline shortages now loom in eastern Germany. The Gas Station Association warns of rising fuel prices, April 22, 2026

- Inosmi.ru: LNG: Turkey opens market to Russia despite EU plans for 2027; BZ: Turkey is considering expanding Russian LNG imports, 04/22/26; Original article: Berliner Zeitung+; Flynn Jacobs: LNG: Turkey opens market to Russia – despite EU ban starting in 2027; 04/21/26

- Finam.ru; Ekaterina Krylova, PSB Center for Analytics and Expertise: The Strait of Hormuz: A Global Logistics Shock in 2026, 04/21/26

- Berliner Zeitung, Anika Schlünz: U.S. Extends Sanctions Waiver for Russian Oil. The U.S. Treasury Department extends an exemption for the purchase of Russian oil. Treasury Secretary Scott Bessent had previously announced the opposite, April 18, 2026

- t-online.de; Analysis by Patrick Diekmann: War in Ukraine. Putin’s Russia is bleeding out, April 17, 2026

Forecasts:

- wiiw: Spring Economic Forecast for Eastern Europe, April 29, 2026

- Interfax.com: Central Bank maintains forecast for Russia’s GDP growth in 2026 at 0.5%-1.5%, at 1.5%-2.5% for 2027, April 24, 2026

- Bank of Russia: Bank of Russia’s medium-term forecast, April 24, 2026

- Bank of Russia: Macroeconomic survey of the Bank of Russia, April 15, 2026

- International Monetary Fund: World Economic Outlook; Global Economy in the Shadow of War, April 14, 2026

- Ostwirtschaft.de: IMF Raises Russia Forecast, April 16, 2026

Weekly and monthly economic reports:

- Politkom.ru; Marina Voitenko; Weekly Report: Global Economy in the Grips of a Supply Shock, April 24, 2026; Budget Deficit Amid Downward Macroeconomic Dynamics, April 16, 2026; Macro trends point to a likely quarterly decline, April 9, 2026

- BOFIT, Bank of Finland; Weekly Review 17/2026: Fixed investment growth in Russia came to a standstill last year; April 24, 2026; Weekly Review 15/2026: Russian GDP growth to remain at last year’s level, boosted by higher commodity prices this year; growth will decelerate in 2027 and 2028, April 10, 2026

- VEB Institute: Global Economy and Markets, April 10–16, 2026; April 17, 2026

Economic data:

- Kommersant; Artem Chugunov: Industry increased production in March, April 23, 2026

- Finmarket.ru: Industrial production in Russia rose by 2.3% in March, April 22, 2026