The World Bank and IMF’s forecasts for Russia differ slightly

Author: Klaus Dormann

The World Bank and the International Monetary Fund released new forecasts on the global economy during their joint spring meeting last week. In mid-January, the two international economic organizations had still been in complete agreement that the Russian economy would achieve 0.8 percent growth in 2026, accelerating to 1.0 percent in 2027.

However, the IMF and the World Bank appear to assess the impact of the sharp rise in energy prices that has since occurred on the Russian economy somewhat differently.

The IMF appears to view Russia more as a “beneficiary” of the rise in energy prices. In any case, it raised its January forecast for Russia’s economic growth this year from 0.8 percent to 1.1 percent. The World Bank, on the other hand, maintained its growth forecast for the Russian economy in 2026, which it had lowered to 0.8 percent in January.

And next year, the World Bank expects Russia’s economic growth to slow slightly further to 0.7 percent. The IMF, on the other hand, anticipates that the Russian economy will grow by 1.1 percent again in 2027.

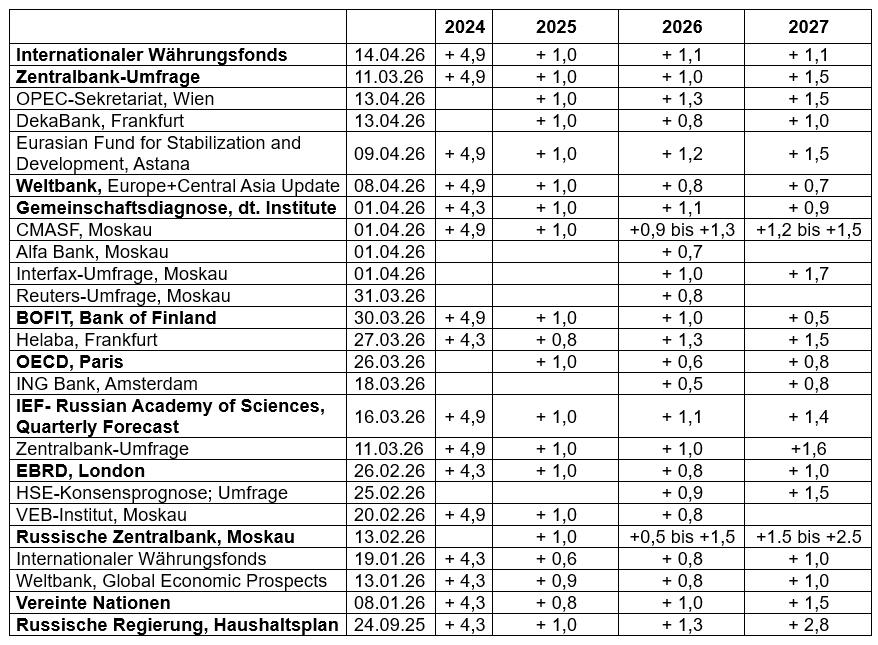

Current growth forecasts for Russia at a glance

However, the difference between the IMF’s and the World Bank’s growth forecasts for 2026 is small, at 0.3 percentage points. At 1.1 percent and 0.8 percent, respectively, the IMF and World Bank forecasts fall roughly in the middle of the 0.5 to 1.5 percent range that the Russian Central Bank cited in February for this year’s growth of the Russian economy. Next Friday, when the Central Bank updates its “Medium-Term Economic Forecasts” in conjunction with its key interest rate decision, it will likely stick to this growth forecast. This is certainly supported by the results of the analyst survey that the Central Bank conducted again in preparation for the key interest rate decision. The survey found that the approximately 30 participants, on average, continue to expect the Russian economy to grow by 1.0 percent in 2026, as it is projected to do in 2025.

GDP Forecasts for Russia 2024–2027

Year-over-year change in real gross domestic product, in percent

World Bank: Russia’s growth to slow slightly further in 2026 and 2027

The World Bank published an update to its “Macro Poverty Outlook” for the Russian Federation on its “Poverty and Inequality Platform (PIP).” In this “country report,” it analyzes economic developments in Russia in greater detail than in its “Europe and Central Asia Economic Update.”

The following excerpt from a table shows that the World Bank expects economic growth in Russia to be only 0.7 to 0.8 percent per year from 2026 to 2028.

World Bank: Real Gross Domestic Product in Russia

World Bank; Poverty and Inequality Platform (PIP):

Country Profile: Russian Federation; Macro Poverty Outlook Russian Federation; April 7, 2026

In summary, the World Bank explains its forecasts for Russia as follows:

The forecasts are subject to considerable uncertainty. They assume a “temporary disruption” in the global energy supply. On an annual average for 2026, prices for Brent crude oil are expected to rise by 36 percent, for natural gas by 67 percent, and for fertilizers by 20 percent.

Real gross domestic product growth is expected to slow to 0.8 percent in 2026. As a result of restrictive monetary policy and higher value-added tax rates, the rise in consumption is slowing.

Fiscal growth incentives are expected to be “limited.” The budget deficit is expected to narrow in 2026 thanks to higher revenues from rising energy prices due to the conflict in the Middle East, and then gradually rise to around 3.4 percent of GDP in 2027–2028.

Average economic growth of 0.7 percent is forecast for 2027 and 2028. Demand pressures will ease due to monetary policy that is expected to remain restrictive. The scope for fiscal growth stimulus is likely to continue to diminish as energy prices fall. The increase in the value-added tax is expected to further dampen consumption.

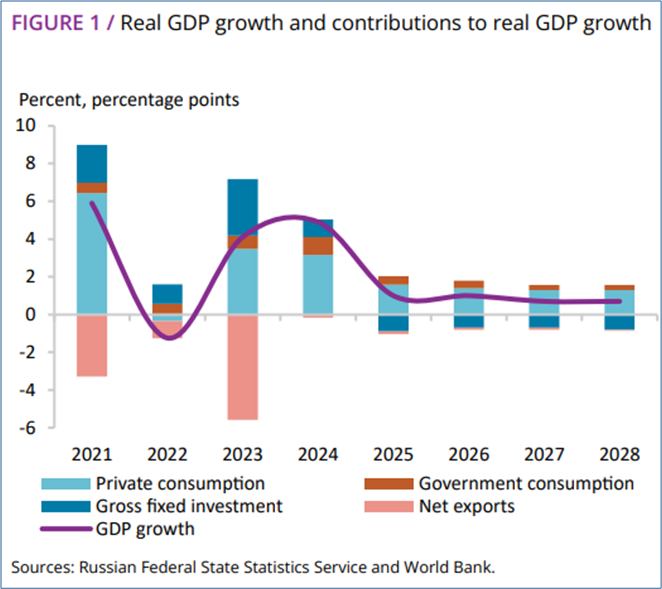

As the following figure shows, however, economic growth over the entire period from 2026 to 2028 will be driven by the rise in private consumption (blue bar segments) and government consumption (dark brown bar segments). By contrast, changes in gross fixed capital formation (dark blue bar segments) and net exports (pink bar segments) are holding back GDP growth.

Real economic growth in percent year-over-year (purple line),

growth contributions of expenditure categories in percentage points

World Bank: Macro Poverty Outlook Russian Federation; April 7, 2026

The pace of the decline in the inflation rate is expected to slow in 2026 due to anticipated strong inflationary pressures from abroad. In the medium term, however, the rise in consumer prices will slow, and the central bank’s inflation target of 4 percent is expected to be reached in 2028. The price-driving external factors will gradually fade away.

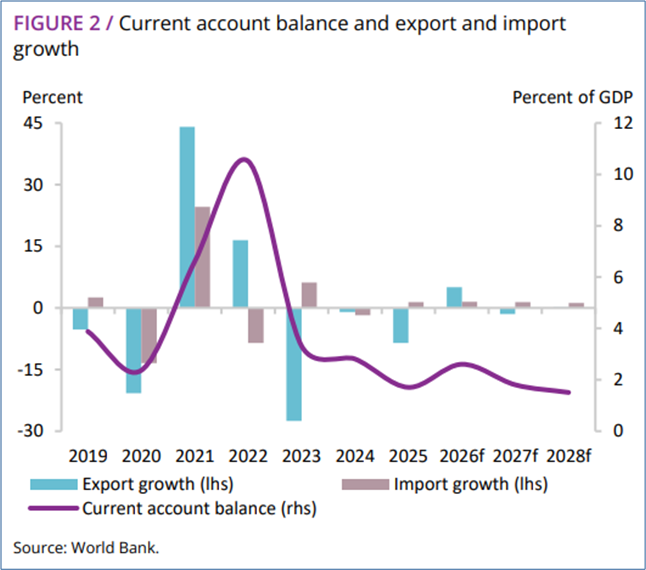

Thanks to higher energy prices, the current account surplus is projected to rise to 2.6 percent of GDP in 2026 (see the purple line in the figure below). In 2027–2028, it is likely to decrease again due to falling energy prices.

External Economic Development: Current Account and Foreign Trade

blue bars: exports; year-over-year change in percent; left scale

gray bars: imports; year-over-year change in percent; left scale purple line: current account balance as a percentage of GDP; right scale

World Bank: Macro Poverty Outlook Russian Federation; April 7, 2026

IMF: Russia’s growth accelerates to 1.1 percent in 2026

Unlike the World Bank, the IMF did not lower its forecast for this year’s growth of the Russian economy last week, but rather raised it from 0.8 to 1.1 percent (see Ostwirtschaft.de). On Friday, the research institute of the state-owned development company VEB.RF reported on the new IMF forecast, summarizing, among other things:

The IMF has revised downward its forecast for global economic growth in 2026 due to the conflict in the Middle East. However, it raised its expectations for Russia’s growth in light of rising energy prices.

In the event of a swift end to the military conflict and a normalization of the oil market by mid-year, global economic growth will amount to

3.1 percent in 2026 (-0.2 percentage points compared to the January forecast; see the first row in the following table from the VEB Institute).

Growth forecasts for this year in most major economies and economic blocs have been lowered (U.S.: -0.1 percentage points; Eurozone: -0.2; UK: -0.5; Canada: -0.1; China: -0.1 percentage points). By contrast, the forecasts for Russia and Brazil were raised significantly (by 0.3 percentage points each).

IMF GDP Forecasts by Country

: Real Gross Domestic Product, Year-over-Year Growth in %;

Changes in GDP Forecasts Compared to January Forecasts in Percentage Points

Institute of the State Development Corporation VEB.RF:

Global Economy and Markets, April 10–16, 2026; April 17, 2026

The IMF’s oil price forecast for 2026 has been revised upward due to transport and production disruptions. The IMF now expects the oil price (arithmetic average of Brent, WTI, and Dubai) to rise by 21% year-over-year to $82 (see also russland.capital).

OPEC Secretariat: Russia’s growth to accelerate to 1.3% in 2026

In its “Monthly Oil Market Report” published in mid-April, the Vienna-based OPEC Secretariat continues to expect Russian economic growth to accelerate to 1.3% in 2026. The Russian government has also forecast this growth rate to date. However, Economy Minister Reshetnikov announced that the forecast is likely to be lowered in April. Regarding the current economic development in Russia, the OPEC Secretariat summarizes, among other things:

Following moderate growth of 1.0 percent in 2025, a slight acceleration of growth to 1.3 percent is expected for 2026. Given the current rise in commodity prices, the Russian economy appears “well-positioned.”

The rise in global commodity prices will have only a moderate impact on inflation due to Russia’s extensive “self-sufficiency” and the government’s ability to impose export restrictions to curb domestic prices.

The rise in commodity prices could provide the government with an opportunity to adjust its fiscal policy accordingly. It will revise this year’s budget planning based on a new macroeconomic forecast, which it will publish in the coming weeks. Furthermore, growth in the Russian economy is expected to be supported in 2026 by further monetary easing and continued stable domestic demand. At the same time, however, “structural constraints”—including persistent labor shortages, capacity bottlenecks, and continued high borrowing costs—are expected to continue weighing on Russia’s growth outlook.

Consumption is expected to be the main driver of growth, supported by continued real wage growth and a corresponding recovery in private lending.

With rising commodity prices, the outlook for capital investment—particularly in the extractive sector—has also improved.

Net exports are expected to make a positive contribution to growth in 2026 and 2027.

Consumer price inflation is expected to continue to ease. A gradual slowdown in domestic demand is likely to dampen price trends this year. The inflation rate is expected to fall below 5% in the second half of 2026.

The central bank cut the key interest rate by another 50 basis points in March, supported by easing inflationary pressures. The central bank is expected to maintain the pace of rate cuts in April and possibly beyond.

Results of the Central Bank Survey on Inflation, Key Interest Rates, and Growth

Ahead of its next key interest rate decision on April 24, the Russian Central Bank conducted another analyst survey from April 10 to 14 (Survey Calendar). The following table shows a selection of the results from this survey.

For the year 2026, the approximately 30 participants expect the following trends in consumer price inflation, the key interest rate, and real gross domestic product growth:

The annual increase in the consumer price index will be 5.5 percent in December 2026, barely lower than a year earlier. By December 2025, the annual inflation rate will have already fallen to 5.6 percent. At the end of 2024, it had reached 9.5 percent.

The annual average inflation rate for 2026 will fall to just 5.6 percent. The annual average for 2025, at 8.7 percent, was still slightly higher than in 2024 (+8.4 percent).

The key interest rate will average 14.1 percent this year, a good 5 percentage points lower than in 2025 (19.2 percent).

Annual economic growth will also reach only 1.0 percent in 2026—the same as in 2025.

Results of the Central Bank survey from April 10 to April 14, 2026

(results of the March survey in parentheses)

Bank of Russia: Macroeconomic Survey of the Bank of Russia, April 15, 2026 (excerpt)

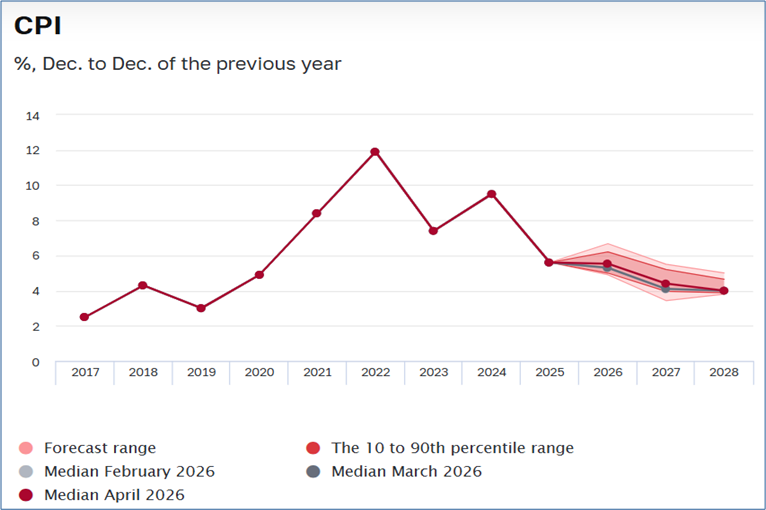

Analysts expect a slower decline in inflation than previously

The following figure shows the projected development of the inflation rate according to the analyst survey. The Central Bank’s target inflation rate of 4.0 percent will not be reached until the end of 2028, based on the average of the survey participants’ estimates (dark red line). According to the survey, consumer prices will still rise by 5.5 percent year-over-year in December 2026. Even by the end of 2027, the inflation target will still be significantly exceeded, with a price increase of 4.4 percent, according to the survey.

Compared to the results of the central bank survey from March (see data in parentheses in the table), analysts’ inflation expectations for December 2026 have risen from 5.3 percent to 5.5 percent. The average inflation forecast for December 2027 rose from 4.1 to 4.4 percent.

Consumer

Price Index: Year-over-year increase in December compared to December of the previous year (in %)

Bank of Russia: Macroeconomic Survey of the Bank of Russia, April 15, 2026

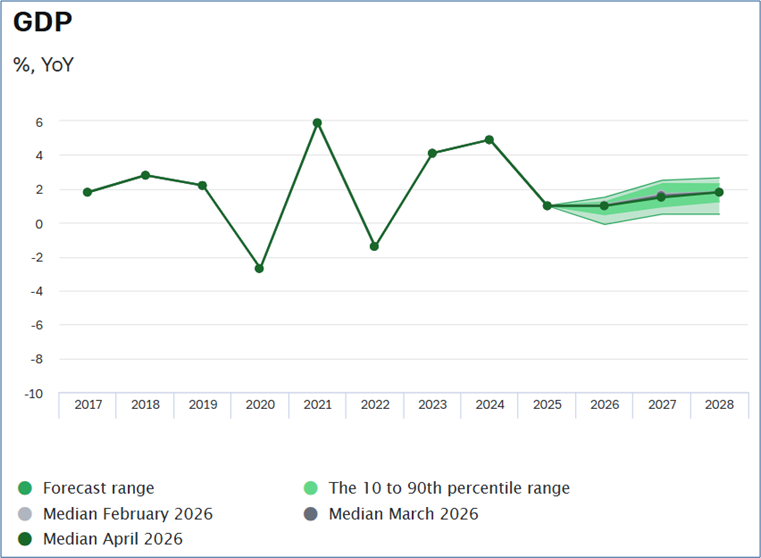

Skeptical growth forecast for 2026: GDP rises by only 1.0 percent

Survey participants’ expectations regarding economic growth have hardly changed since the December survey. In 2026, with a projected GDP increase of 1.0 percent, they continue to expect growth to remain as low as it was in 2025. Analysts thus apparently do not expect the sharp rise in energy prices to accelerate economic growth, but rather, at best, to stabilize it.

They do, however, anticipate GDP growth picking up to 1.5 percent in 2027 and 1.8 percent in 2028. However, starting in 2027, the analysts’ growth forecasts remain well below the government’s previous projections, which anticipate growth rates of 2.8 percent and 2.5 percent in its 2027 and 2028 budget plans.

Real Gross Domestic Product

Year-over-year change in percent

Bank of Russia: Macroeconomic Survey of the Bank of Russia, April 15, 2026

President Putin is also not spreading “growth optimism”

In an opening speech at consultations with government officials on the development of the Russian economy on April 15, President Putin highlighted the current decline in aggregate economic output during the first two months (en.kremlin.ru). He stated:

“Overall, GDP declined by 1.8% in January and February. The manufacturing sector and industrial production as a whole suffered output losses, as did a sector as systemically important as the construction industry.”

Putin did note once again that weather conditions contributed to the slowdown in economic growth during the two winter months. Additionally, this year’s January had two fewer working days and February one fewer working day than in 2025. However, the president also emphasized:

“I expect detailed reports today on the current economic situation and on why the development of macroeconomic indicators is currently falling short of expectations. Economic performance is lagging not only behind the expectations of experts and analysts, but also behind the forecasts of the government and the Central Bank of Russia.”

He expects proposals on what additional measures need to be taken to ensure the growth of the Russian economy (russland.capital with video and German translation of Putin’s speech; Die Presse, Berliner Zeitung+; Vedomosti; BBC video: Rosenberg Press Review).

Kremlin spokesman Dmitry Peskov reported the following day on the deliberations, noting that the closed-door portion of the meeting had lasted several hours. Numerous proposals had been made to stimulate the economy. However, Peskov declined to provide details, according to a Reuters report. Participants included Prime Minister Mikhail Mishustin, Deputy Chief of Staff of the Presidential Administration Maxim Oreshkin, First Deputy Prime Minister Denis Manturov, Deputy Prime Minister Alexander Novak, Central Bank Governor Elvira Nabiullina, and PSB Bank CEO Pyotr Fradkov.

Many experts expect lower GDP in the first quarter than a year ago

Vedomosti surveyed several well-known analysts on the expected development of aggregate economic output in the first and second quarters.

In the first quarter of 2026, they anticipate a year-over-year decline in real gross domestic product of 0.5 to 1.5 percent or near-stagnation in overall economic output. Alexander Shirov, director of the Institute for Economic Forecasting at the Russian Academy of Sciences, is particularly skeptical about current growth trends. He believes that the “economic slowdown” has affected more and more Russian companies and is triggering a “domino effect.” While pent-up demand could support production growth, Shirov assumes that this would only be possible if the key interest rate were lowered more quickly than is currently the case. He expects overall economic output to decline by 1% to 1.5% in the first quarter. For the second quarter, he forecasts merely “zero growth.”

According to Yegor Susin, head of Gazprombank’s Center for Market Strategies, economic growth is falling short of forecasts not only due to one-off calendar effects but also due to tax hikes. The impact of the increased budget spending at the start of the year will only become apparent in the second half of the year.

At the same time, Susin notes that there will be three more working days in the second quarter. He sees no risk of recession. Rising prices for Russia’s exports would provide additional support for production growth in the second quarter. Shirov also expects growth in foreign trade revenues in April and May.

Marina Voitenco: Economic activity is currently “below freezing”

Marina Voitenco, a long-time “economic policy observer” for the Russian website Politcom.ru, provides the following overview of the current economic situation in her latest weekly report:

“Following a 1.8% decline in GDP in January and February, most experts expect negative GDP growth in the first quarter, with declines ranging from 0.8% to 1.5%. Only a few estimates predict growth close to zero or a slight increase (up to 0.2 to 0.4%). Investment is likely to continue to decline… .

In the second quarter, the situation will gradually improve thanks to exports (primarily due to rising energy and fertilizer prices). Nevertheless, uncertainty regarding the outlook for global economic development remains extremely high. The timing of an end to the conflict in the Middle East is uncertain. Risks of escalation and a deterioration in international trade and the global economy as a whole persist. …

The currently projected growth rate of Russian GDP in 2026 averages around 1%. However, the share of forecasts close to zero is also rising.

This year’s actual growth rate will depend largely on the coordinated efforts of the government and monetary authorities to reduce price growth to about 5% year-over-year and to create the conditions for investments aimed at increasing labor productivity.”

Finance Minister Siluanov: The federal budget deficit will soon disappear

At the Moscow Stock Exchange Forum on April 16, Russian Finance Minister Anton Siluanov commented on the federal budget’s development during a panel discussion with Economy Minister Reshetnikov and Central Bank Governor Nabiullina. He expressed confidence: There is no need to worry about the current budget deficit, as it was foreseeable. Because oil and gas revenues declined in the first quarter, total revenues fell slightly in the first quarter. Everyone is aware of the current trend in energy prices. The federal budget deficit will be balanced within a year.

Regarding the ruble’s exchange rate, Silunaov noted that the exchange rate would remain stronger “than many would like” for several years. A strong exchange rate poses a “structural challenge” for the Russian economy. To overcome this, flexibility is needed in the labor market and in the management of insolvencies.

Central Bank President Nabiulla pointed out that, for the first time in the history of modern Russia, there is a labor shortage (Berliner Zeitung). The Central Bank’s forecast that the inflation rate will fall to 4.5 to 5.5 percent by the end of 2026 takes into account a temporary rise in inflation at the beginning of 2026. The Russian Central Bank is not aiming to reduce the inflation rate to 4 percent at any cost (Vedomosti.ru).

Recommended reading:

War, energy supply, energy prices, and Russia:

- t-online.de; Analysis by Patrick Diekmann: War in Ukraine. Putin’s Russia is bleeding out, 04/17/26

- Die Presse+; Interview by Eduard Steiner with Vladislav Inozemcev: “If the West wants regime change in Russia, it must lift sanctions,” Inozemcev explains, among other things, why the billions in revenue from high oil prices are of little help to Russia, April 17, 2026; Euromaidan Press interview by Peeter Helme: Vladislav Inozemtsev: A collapse is not imminent. Inozemtsev on oil windfalls, Ukrainian strikes, and why the war will be won on the ground, April 10, 2026

- “Die Presse” podcast on the Russian economy: Price shock for oil and gas. Will Europe soon have to buy from Russia again? Eduard Steiner and Russia economist Vasily Astrov (WIIW) in conversation with international energy consultant Johannes Benigni, April 15, 2026

- Phoenix Roundtable: Trump’s naval blockade—a debacle for the whole world. Anke Plättner discusses with: Hartwig Ross, expert on maritime security; Bente Scheller, Heinrich Böll Foundation; Prof. Rüdiger Bachmann, German-American economist; Reza Asghari, CDU Member of the Bundestag, April 15, 2026

- Markus Lanz: Energy Crisis: Does the Government Have No Plan? DIW energy expert Prof. Claudia Kemfert criticizes the federal government for acting with short-term, unfocused measures. Journalist Michael Bröcker, editor-in-chief of “Table Briefings,” shares this view; 04/15/26

- Inosmi.ru: Hungary’s new prime minister will have a hard time saying “no” to Russian oil and gas; original article: Sohu, China, April 13, 2026.

- Berliner Zeitung, Flynn Jacobs: EU buys more Russian LNG – now the Eni CEO is calling for sanctions to be postponed.Due to the Hormuz crisis, the Eni CEO is calling for the LNG ban against Russia to be postponed until 2027, April 13, 2026; see also Inosmi.ru, April 14, 2026

- Forbes.ru; Elena Khudaeva: Analysts have examined the impact of the war in Iran on Russia’s economic growth, April 13, 2026

- Kommersant; Artem Chugunov: Analysts examine the Strait of Hormuz. The war in the Middle East is having its first effects on macroeconomic forecasts for Russia, April 12, 2026

- Natalia Asedova, Finam.ru: On the Brink of a Severe Crisis. What Are the Consequences of the Blockade of the Strait of Hormuz? 04/13/26

Fiscal Policy; National Budget and Oil Prices:

- BondGuide; Alexander Kolyandr and Alexandra Prokopenko (THE BELL): Russia wastes no time with high oil prices: but spending is still outpacing revenue, 04/17/26

- Focus.de; Lars-Eric Nievelstein: Russia’s budget deficit hits annual target after just three months. Russia’s economy is under pressure. Revenues are weakening significantly. 04/17/26

- Politkom.ru; Marina Voitenko: Budget deficit amid downward macroeconomic trends, 04/16/26

- Finam.ru; Olga Belenkaya: The planned annual budget deficit has already been exceeded, 04/09/26

Overall economic development:

- Interfax.com: The Russian economy’s reserves are largely depleted; the macroeconomic situation is more difficult than in recent years – Reshetnikov, 04/17/26

- LIGA.net news editor Vira Kasiyan: Russia admits that the economy’s reserves are “nearly exhausted.” The Minister of Economic Development of the Russian Federation stated that the macroeconomic situation is significantly more difficult than in previous years, 04/17/26

- Global Banking & Finance Review®: Top Officials Have Offered Putin Ideas for Economic Growth After Contraction, Kremlin Says, April 17, 2026; Reuters; Guy Faulconbridge, Dmitry Antonov, and Elena Fabrichnaya: Russia looks for a way out of its sharpest economic contraction in three years, April 16, 2026

- Berliner Zeitung, Liudmila Kotlyarova: Central Bank Sounds the Alarm: Russia Faces Labor Shortage “for the First Time.” Ukraine Invasion Exacerbates Labor Shortage: Central Bank Chief Nabiullina Sees Russia’s Economy at Its Limit—Despite High Energy Revenues, 04/16/26

- The Moscow Times: Putin Demands Answers as Russia’s Economy Falls Short of Expectations, April 15

- The Moscow Times; Vasily Burov, consulting firm Estonto Lab; Andrei Yakovlev, Davis Center at Harvard University: Ending the war in Ukraine will not fix Russia’s economy, April 15, 2026

- Vedomosti; Ksenia Kotchenko: Putin ordered an explanation for the discrepancy between government forecasts and GDP data. Experts see the reasons not only in calendar and seasonal factors, April 16, 2026

- Vedomosti; Valeria Khlobystova: What Nabiullina, Reshetnikov, and Siluanov said at the stock market forum about the budget, interest rates, and the IPO of state-owned companies. The finance minister assured that the budget deficit would be balanced within a year, 04/16/26

- MK.RU; Vladimir Chuprin: Russia’s economy ranks fourth in the world: Is that good or bad? Interview on Russia’s economic growth with Igor Nikolaev, Institute of Economics of the Russian Academy of Sciences, April 16, 2026

- Vedomosti: Russia remains the world’s fourth-largest economy in terms of purchasing power parity (PPP), 04/16/26; Ntv.ru: Russia retains fourth place globally in terms of GDP, 04/16/26

- russland.capital: Putin calls for measures against slowing economic growth, 04/16/26; with video (with German translation): Putin held a meeting on economic issues, 04/15/26

- Vedomosti.ru: Putin: The economy has contracted more than the government and central bank had forecast. The president called for measures to stimulate growth, April 15, 2026; Regnum.ru: Putin reported a 1.8% decline in Russian GDP over the past two months. April 15, 2026

- Die Presse: Russia’s national budget. “I expect proposals”: Russia’s economic slump puts pressure on Putin, April 15, 2026

- Alexandra Prokopenko in an interview with Tagesanzeiger.ch; Clara Lipkowski: War in Iran: Alexandra Prokopenko on Russia’s economy, 04/15/26

- nd-aktuell.de; Hermannus Pfeiffer: Russia in the shadow of sanctions. Thanks to stimulated domestic demand, Russia’s economy remains surprisingly stable after four years of war, aided by rising oil prices. 04/14/26

- Monocle.ru; Charts: The GDP index has returned to the level of a year ago. Export prices for Russian raw materials rose by 41% in March. The budget deficit is growing faster than in previous years, April 13, 2026

- Alexander Shirov, Director of the IEF-RAS: “The Economy of Chance.” What opportunities do global changes present for Russia? Vedomosti, April 13, 2026

Forecasts:

- Bank of Russia: Macroeconomic Survey of the Bank of Russia, April 15, 2026

- International Monetary Fund: World Economic Outlook; Global Economy in the Shadow of War, April 14, 2026

- Ostwirtschaft.de: IMF Raises Russia Forecast, April 16, 2026

- russland.capital: Rising commodity prices: IMF raises forecast for Russian GDP growth, April 15, 2026

- Der Standard, András Szigetvari: IMF Forecast. How Trump’s War Against Iran Makes Russia Richer and Europe Poorer, April 14, 2026

- Die Zeit: International Monetary Fund: IMF lowers forecasts for Germany and the global economy, April 14, 2026

- Finmarket.ru: The IMF has lowered its forecast for global GDP growth in 2026 to 3.1%, April 14, 2026

- Interfax.ru: The IMF has lowered its forecast for global GDP growth in 2026 due to the Iran conflict, April 14, 2026

- Kommersant, Artem Chugunov: Experts believe the risk of recession is low. Rosstat has revised the quarterly GDP growth rates for 2025: 04/14/26

- Eurasian Fund for Stabilization and Development, Astana: EFSD Regional Economic Outlook Spring 2026, April 9, 2026

- IEF RAS: Analysis of Short-Term GDP Dynamics: April 2026, April 8, 2026

- World Bank: Europe and Central Asia Economic Update – April 2026, Summary, April 8, 2026

- World Bank; Poverty and Inequality Platform: Country Profile: Russian Federation;

Macro Poverty Outlook Russian Federation; April 7, 2026