To what extent and for how long will Russia benefit from the energy price boom?

Author: Klaus Dormann

Since the start of the Iran war about a month ago, oil and gas prices have risen sharply worldwide. Analysts are developing scenarios on how higher energy prices could affect economic growth and inflation in Russia. Russia is often seen as the real “beneficiary” of the Iran war, as its sharply fallen export revenues and government revenues are expected to rise significantly.

However, the BOFIT research institute of the Bank of Finland emphasizes in its weekly report that a rise in energy prices lasting only a short time could improve the state of the Russian economy only to a limited extent. BOFIT will publish its new forecast for Russia for the period 2026–2028 on March 30.

Last Wednesday, the Paris-based “Organization for Economic Cooperation and Development (OECD)” presented new forecasts for global growth and inflation in its “Economic Outlook Interim Report.” The OECD expects that prices for oil, gas, and fertilizers “will gradually decline again starting in mid-2026.”

British analyst Timothy Ash points out that an excessively long and sharp rise in energy prices also poses risks for Russia. Global demand could then collapse, leading to an economic disaster in Russia as well, Ash writes in the Kyiv Post.

In the eurozone, higher energy costs are slowing growth and driving inflation

Given the global rise in energy prices so far, the OECD now expects higher inflation and lower growth in the eurozone countries, because:

“The sharp rise in energy prices and the unpredictable course of the conflict in the Middle East will increase costs and dampen demand.”

The OECD has significantly lowered its growth forecast for eurozone countries by 0.4 percentage points to 0.8 percent. It now expects growth of just 0.8 percent for the two largest EU economies, Germany and France, as well. At the same time, the OECD raised its inflation forecast for the eurozone by 0.7 percentage points to 2.6 percent in 2026.

According to the OECD, the surge in energy prices is barely boosting growth in Russia

Despite the sharp global rise in energy prices, the OECD raised its growth forecast for Russia’s energy-intensive economy only slightly. It now expects real gross domestic product in Russia to rise by 0.6 percent for the full year 2026. That is only 0.1 percentage points more than three months ago in December. The OECD raised its forecast for Russia’s GDP growth next year by 0.2 percentage points to 0.8%.

Accordingly, Russia will apparently receive only relatively weak growth impulses from the sharp rise in energy prices, even though the country is one of the world’s leading energy exporters (bpb; Statistical Review of World Energy). However, it is important to note that without Russia’s export-driven energy sector, economic growth in Russia would likely be impacted just as severely by the current rise in energy prices as, for example, growth in the energy-poor countries of the Eurozone.

According to the OECD, Russia will also feel the impact of rising energy prices caused by the war in Iran through an accelerated rise in consumer prices. Russia’s inflation rate will remain noticeably higher than the OECD had previously expected. According to the new OECD forecast, it will only decline from 8.7 percent in 2025 to 6.4 percent in 2026. In December, the OECD had forecast a decline in the inflation rate to 5.4 percent for 2026.

BOFIT: Growth in the Russian economy has come to a standstill

According to an assessment by the BOFIT research institute of the Bank of Finland, the state of the Russian economy has deteriorated significantly in 2026. A short-term rise in oil prices is not sufficient to reverse this trend. Furthermore, the government’s fiscal policy space has not yet expanded significantly.

BOFIT published the following chart on the development of production in the five “core sectors” of the Russian economy and the Russian Ministry of Economic Development’s estimates of overall economic production based on these figures. It shows that both the annual growth of real gross domestic product (blue line) and the annual growth of output in the core sectors of the economy (green line) have fallen to around zero percent in January 2026, based on a 3-month moving average.

Growth in Russian production has come to a standstill

BOFIT, BOFIT Weekly: Higher oil prices bring at least temporary relief for the Russian economy, March 27, 2026

The government plans to lower its growth forecast of 1.3 percent for 2026

Regarding economic developments in February, the statistics agency Rosstat reported that industrial production in the period from January to February 2026 fell by 0.8% compared to the first two months of the previous year. Adjusted for seasonal and calendar factors, Russian industry grew by 0.3% in February 2026 compared to the previous month, according to Rosstat, after stagnating in January (Finmarket.ru).

Economy Minister Maxim Reshetnikov announced on the sidelines of an economic conference last week that the government will lower its previous forecast for this year’s Russian economic growth from 1.3 percent in April. Reshetnikov stated: “We had expected a difficult first half of the year. And that is exactly how it turned out.” The minister also emphasized that the Central Bank’s monetary easing would have no immediate impact on the economy. “It is clear that the interest rate cut has a delayed effect and will hardly influence the situation in 2026,” he said (vz-nn.ru).

Business surveys show the deteriorating state of the economy

BOFIT points out that the deteriorating state of the Russian economy was also reflected in surveys of Russian companies:

In the Russian Central Bank’s monthly survey, companies’ assessment of the economic situation this year has deteriorated significantly. In March, companies rated the current situation as nearly as weak as in the spring of 2022, immediately following Russia’s invasion of Ukraine (see also Politkom.ru weekly report).

In other business surveys as well, the majority of respondents stated that their company’s situation had deteriorated in the first half of the year or would deteriorate in the coming months.

Among the problems cited by companies are rising costs and payment arrears. For example, in a survey conducted by the RSPP industry association at the end of 2025, payment arrears were the most frequently cited problem. More than 40% of companies—a higher percentage than during the COVID-19 pandemic—reported that payment arrears were affecting their business.

Rising oil prices bring higher revenues and stimulate growth

Nevertheless, BOFIT believes that the situation of the Russian economy at the beginning of 2026 has “at least temporarily eased” in light of the sharp rise in global oil prices. The rise in world market prices has benefited the development of Russian oil exports. In addition, U.S. sanctions against Russian oil exports have been eased.

BOFIT points out that higher oil prices generally stimulate Russian economic growth and boost export revenues and government revenues. According to BOFIT, oil and gas still accounted for more than half of Russia’s goods exports and nearly a quarter of federal budget revenues in 2025.

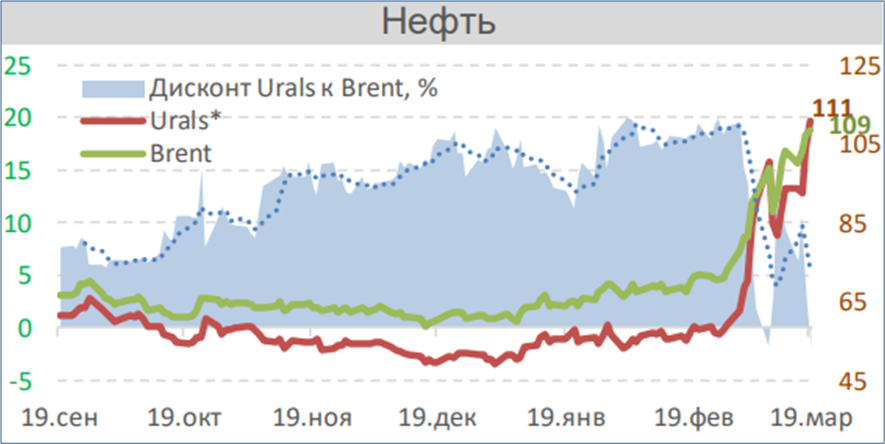

The Urals oil price rose by about two-thirds in March compared to February

BOFIT cites the following data regarding oil price trends:

The average price for a barrel of Brent crude rose to around $96 in March 2026.

According to Bloomberg estimates, the price of a barrel of Russian Urals oil has also risen significantly in recent weeks to around $60.

The following figure from the weekly report of the research institute of the Russian state development corporation VEB.RF compares the sharp rise in the prices of Urals and Brent crude. According to the data, the price of Russian Urals crude, at $111 per barrel on March 19, even narrowly exceeded the price of Brent crude at $109 per barrel, according to Cbonds (The research institute notes, however, that Cbonds’ data differs from price figures from other sources).

Oil price trends from September 19, 2025, to March 19, 2026

Blue bars: Urals discount relative to Brent in %

VEB.RF Weekly Report: Global Economy and Markets, March 20, 2026

For daily oil price trends, see also: Trading Economics: Urals Oil. According to Trading Economics, the Urals price rose by 66.5 percent last month compared to the previous month (as of March 25, 2026).

Oil and gas revenues in the federal budget have halved so far in 2026

BOFIT reports on the development of the Russian federal budget at the beginning of 2026:

Russia’s budget plan for 2026 is based on the assumption of an average export price of $59 per barrel. In January and February of this year, the average export price for Russian oil was just $46 per barrel, according to estimates by the International Energy Agency (IEA), compared to $65 per barrel in the previous year. The average discount for Russian oil relative to benchmark grades reached $23 per barrel in January and February, while it was only $13 per barrel in 2025. The IEA also estimates that oil export volumes declined, particularly in February (for more information: IEA Oil Market Report).

According to preliminary data from the Russian Ministry of Finance, total revenues in the Russian federal budget fell by about 10 percent in January and February compared to the previous year.

The trend in total revenues was particularly hard hit by a drastic decline in revenues from the oil and gas sector, which were nearly 50 percent lower than in the previous year. The main reason for this was the significant drop in the export price of Russian oil.

Federal budget revenues excluding revenues from the oil and gas sector rose by 4% in January and February compared to the previous year. This increase is attributable to the two-percentage-point VAT hike that took effect at the beginning of the year. As a result of the increase, VAT revenues rose by 11% year-over-year, while other revenues fell by 5%.

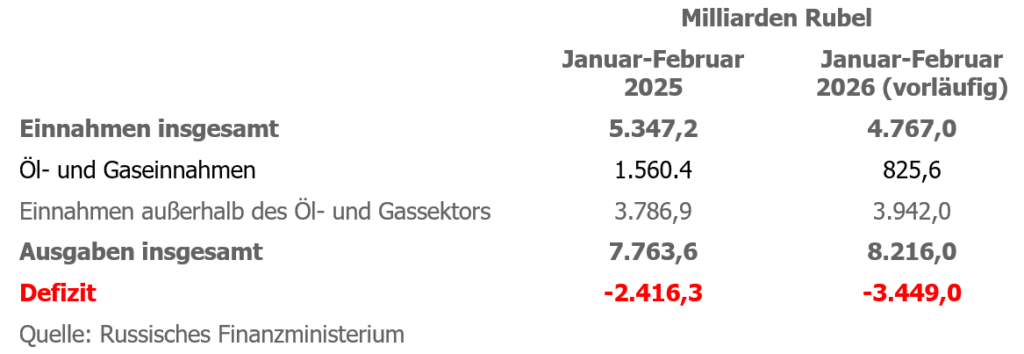

The “Economic Expert Group,” a research institute that works closely with the Russian Ministry of Finance, published the following table (excerpt), among other data, on the development of revenues, expenditures, and the deficit of the Russian federal budget in the first two months of 2026.

Development of the Federal Budget in January–February 2026

Economic Expert Group: Economic Analysis March 2026 (excerpt), March 25, 2026

Federal budget expenditures rose by 6% in January and February compared to the previous year. They grew slightly faster than planned for the full year, while revenues fell short of expectations.

The federal budget deficit in January and February nearly reached the level projected for the entire year of 2026. It amounted to approximately 3.4 trillion rubles (1.5% of GDP).

According to BOFIT, this year’s budget deficit is to be financed primarily through borrowing via government bonds. However, a total of around 400 billion rubles was withdrawn from the “National Welfare Fund” in January and February to cover the deficit. At the end of February, the fund still had liquid assets worth around 4 trillion rubles.

Vasily Astrov: “The war in Iran came at exactly the right time for Russia”

With this headline, the Austrian newspaper “Die Presse” draws attention to the latest episode of its podcast on the Russian economy. Longtime Russia correspondent Eduard Steiner spoke with Vasily Astrov, the Russia expert at the “Vienna Institute for International Economic Comparisons,” on March 25, among other things, how the Russian state budget has developed and what prospects are emerging for the Russian economy in light of rising energy prices (minutes 19 to 31).

Astrov summarizes the budget development as follows:

Russia is now, of course, earning much more from its oil exports than it was a month ago. For one thing, global oil prices have risen sharply. In addition, the price discount for Russian oil relative to Brent crude has narrowed significantly.

However, Russia’s immediate priority is to use the higher revenues to plug holes in the budget. Before the start of the war in Iran, the budget situation was, from Russia’s perspective, “truly alarming.” A budget deficit of 1.6 percent of gross domestic product had been planned for the full year 2026. However, the deficit was already so high after the first two months of 2026 that the deficit ratio targeted for the full year 2026 had been reached. From this perspective, the Iran War and the sudden rise in global oil prices—and to some extent gas prices as well—came at just the right time from Russia’s point of view.

However, it is not the case that Russia is suddenly “swimming in money.” The Russian government will use the additional revenue to plug the holes in the state budget. It will then have to borrow less.

Looking ahead, much will of course depend on how long the high energy prices actually persist.

Across-the-board spending cuts of 10 percent are off the table for now

Astrov also reported on announced spending cuts:

Three days before the start of the war in Iran, the Russian finance minister announced a 10 percent cut in all government spending. The only exceptions were to be spending on the military, social spending, and the salaries of public sector employees.

However, these austerity plans have now been temporarily “put on hold.” The spending cuts will be postponed, likely until 2027 (see also The Moscow Times).

High energy prices do “little” to help economic growth

Vasily Astrov believes that the rising government revenues driven by energy prices can certainly contribute to lower budget deficits. However, he considers the impact of higher energy prices on “the economy as a whole” to be “rather small.” He states, among other things:

At the moment, the Russian economy is stagnating; there are even signs of a recession. According to an estimate by the Ministry of Economic Development, GDP fell by about two percent year-over-year in January.

According to a business survey by the Russian Central Bank, the business climate fell in March to its lowest level since October 2022. The business climate is thus as poor as it was at the time when the Russian economy was suffering from the shock of the sanctions.

From Russia’s perspective, the overall economic situation is therefore “not rosy.” The main cause of this is the persistently high interest rates. The rise in energy prices and Russia’s additional revenue are “not necessarily” helping to solve these problems.

Timothy Ash: Russia urgently needs the rise in energy prices. In the long term, however, the war in Iran poses risks for Russia

British economist Timothy Ash, “Associate Fellow in the Russia and Eurasia program at Chatham House” and “Senior Sovereign Strategist at RBC Bluebay Asset Management” in London, analyzed the potential consequences of the war in Iran for Russia in an opinion piece published by the “Kyiv Post.”

He concludes that while “the third Gulf War” would bring Russia financial benefits in the short term, it also carries risks in the long term. Below is a summary of what Ash writes regarding the decline in Russian oil export revenues and the decline in government revenues from the oil and gas sector to date:

The “third Gulf War” has driven up energy and commodity prices.

Combined with the U.S. decision to ease sanctions against Russia, this will cause Russia’s export revenues to rise. The Russian state coffers will fill up. The war against Ukraine and Europe can thus continue longer than would otherwise have been the case.

Russia’s oil export revenues fell to a four-year low in February

Over the course of 2025, sanctions against Russia were further tightened. In the first months of 2026, Russia’s revenues from energy exports and energy-sector revenues in the Russian state budget fell significantly.

According to IEA data, for example, revenues from oil and petroleum product exports fell by $1.5 billion in February 2026 to just $9.5 billion. This is the lowest level since the start of the war in Ukraine in 2022.

The decline in revenues reflected, on the one hand, an increase in the price discount on Russian oil to over 30%. In addition, Russian oil export volumes fell to 6.6 million barrels per day in February, a decline of 850,000 barrels per day compared to the previous month and also the lowest level since 2022. Export volumes appear to have fallen due to both Western sanctions and successful Ukrainian drone and missile strikes on Russian energy infrastructure.

Russia’s trade surplus fell by over 10% in January 2026 compared to the same month the previous year, dropping to just $6.5 billion.

Government revenues from the oil and gas sector fell sharply

In the federal budget, oil and gas revenues fell by 44% year-over-year in the first two months of the year. The budget deficit rose to 1.5% of GDP, even though the government had raised the value-added tax from 20% to 22% at the start of the year. The media reported that spending cuts of 10% were being planned.

Russia’s government thus found itself facing an increasingly strained fiscal situation. Falling revenues were offset by rising military spending. Since reserves in the “National Welfare Fund” had been depleted, the government had to cover a larger budget deficit through increased domestic debt.

This measure meant higher interest rates, further crowding out of the civilian sector, and likely rising inflation, which in turn would keep key interest rates high and dampen growth.

The Russian economy was already on the brink of a recession

Real gross domestic product contracted in the first months of 2026. Forecasts for economic growth for the year as a whole were close to zero.

The economy increasingly resembled a two-tier society: The military-industrial sector continued to benefit from increased defense spending and its prioritization, while the rest suffered from high inflation, labor shortages, high labor costs, high debt, and high interest rates.

Ash: The U.S. war in Iran initially gave Putin a “major victory”

Ash assesses the U.S. government’s decision to attack Iran as follows:

“Just as the economic downturn seemed to be forcing Putin to make difficult decisions—such as concessions in the Ukraine peace talks—Trump handed Putin a major victory with his bizarre decision to attack Iran without any discernible, well-thought-out strategy. In the short term, this will serve as a free pass for Putin. Higher oil and energy prices, as well as the U.S. decision to ease sanctions on Russian oil, will strengthen Russia’s budget and balance of payments.”

Ultimately, however, oil and commodity prices could plummet

Ash estimates that Russia’s oil and energy revenues could initially increase by up to $10 billion per month. At the same time, however, he points out that the long-term consequences of persistently high oil prices remain unclear. Presumably, persistently high oil prices will lead to a slump in demand and lower global growth, similar to the period around COVID-19 or during the 2008 global financial crisis. Russia would then be the one to suffer the consequences. Higher oil prices in the long term could trigger “a disaster” for the Russian economy.

Recommended reading:

- German-Russian Chamber of Foreign Trade:

Analyses, German; also Russian; (selection):

Growth, Key Interest Rate, Ruble Exchange Rate: Forecasts in Light of the Iran War, 03/23/26Hormuz Shock: Europe Facing a New Gas Crisis, 03/18/26Hormuz Shock: How Big Will Russia’s Unexpected Oil Windfall Be? March 11, 2026Economic Consequences of the War in Iran: Oil Price, Russia, Tourism; March 2, 2026Weak Growth, Dwindling Reserves, and High Military Spending, February 18, 2026 - Podcast “Tsars, Data, Facts” by the German-Russian Chamber of Foreign Trade, hosted by Thomas Baier:

Russia’s Economy: Sanctions and Growth Prospects; Guest: Prof. Jacques Sapir, 44 min., 03/09/26 Low Gas Storage Levels: Europe’s Challenge in the Energy Market; Guest: Dr. Heiko Lohmann, “energate Gasmarkt”; 34 min., 03/01/26 - “Die Presse” podcast on the Russian economy: Russia – Gas, Sanctions, Oligarchs:

Expert Vasily Astrov points out: “The war in Iran came at exactly the right time for Russia”; recorded on 03/25/26; The podcast guest is military expert Wolfgang Richter, a retired German colonel. He explains how the war in Iran will also change the war in Ukraine; 48 min., 03/27/26

Is Russia the big winner of the war in Iran and China the loser? Recorded on March 10, 2026;

The war in Ukraine has made Russia the economic loser and China the beneficiary. The war in Iran, however, has entirely different implications. Vladimir Putin is already laughing up his sleeve. And China? Professor of Sinology Dr. Susanne Weigelin-Schwiedrzik and Russia economist Vasily Astrov (WIIW) in conversation with Eduard Steiner; March 11, 2026

The Iran War, Energy Supply, and Russia

- Inosmi.ru; Bloomberg: The Trump administration is analyzing the consequences of a possible rise in oil prices to $200 per barrel, March 26, 2026

- Inosmi.ru; Bloomberg: Russia sold 60 million barrels of oil to India, delivery in April, March 25, 2026

- Kyiv Post; Timothy Ash: OPINION: For Russia – Gulf War 3 Creates Economic Wins but Also Risks, March 24, 2026

- Fortune; Marco Quiroz-Gutierrez: Putin is the real winner in Trump’s Iran war as it puts Russian oil back on the map, March 23, 2026

- Focus.de; Analysis by Ulrich Reitz: Putin Deal? Overshadowed by the Iran War, an Explosive Idea Is Circulating, March 22, 2026

- FR.de; Marcus Giebel: Hundreds of billions of dollars: How Putin could profit from the Middle East war – three scenarios. Study by the “Kyiv School of Economics” (KSE); March 21, 2026

- Kyiv School of Economics: Iran war helps Russia; a long conflict would fundamentally undermine the economic pressure campaign; easing sanctions does not resolve energy market challenges — KSE Institute, Study: Assessment of the Impact of the Iran War on Russia, March 20, 2026

- Foreign Policy Podcast “Ones and Tooze,” Ep. 234: Adam Tooze on the Economic Fallout of War in Iran (plus: Jürgen Habermas), March 20, 2026

- Jacques Sapir, Director of the CEMI (Center for Industrialization Studies, Paris), foreign member of the Russian Academy of Sciences; Kommersant: Global Economic Crossroads. Three Scenarios for the Middle East Conflict; March 19, 2026

- BBC; Dharshini David, Deputy Economics Editor: Russia, China, and the US – the Global Winners and Losers of the Iran War, March 19, 2026

Fiscal Policy: National Budget and Oil Prices

- Moscow Times: Russia Drops Budget Cut Plans as Oil Price Surge Boosts Revenues – Bloomberg, March 27, 2026

- Yahoo Finance; Reuters: Russia delays change to fiscal fund after Iran war energy price surge, March 23, 2026

- Inosmi.ru; Stratfor USA: Ironically, Russia is benefiting from the Iran-related oil price shocks. Stratfor: A US war against Iran will lead to a Russian budget surplus, March 23, 2026

- Politkom.ru; Marina Voitenko: Extremely high volatility in oil prices and extremely uncertain consequences, March 19, 2026

- Deutsche Welle.com/ru; Oleg Loginov: SIPRI: Russia has passed the peak of military spending growth, March 19, 2026

Overall economic development:

- ura.news: Russia faces a year without economic growth. Expert Nikolayev cited five reasons for the economic crisis in Russia, 03/24/26

- ura.news: Nothing catastrophic will happen, but the situation on the labor market will worsen, noted Igor Nikolaev. Russia’s economic statistics increasingly point to a recession, according to Igor Nikolaev, a leading researcher at the Institute of Economics of the Russian Academy of Sciences, March 24, 2026

- Anadolu Agency; Kanyshai Butun: Russia says EU energy restrictions could cost the bloc over $3.48 trillion by 2026. Moscow envoy says EU losses already top $1.74 trillion as gas price surge hits the economy, March 23, 2026

- Le Monde; Stéphane Lauer: “The oil shock in the Middle East is a godsend for Russia,” March 23, 2026

- ntv.de: Decisive measures called for. Putin acknowledges slump in Russian economy, 03/23/26; Der Spiegel: Russia’s economy slips into negative territory—even Putin now sees it, 03/23/26

- RBC.ru, Ekaterina Kuzmina: Putin considered the decline in GDP in January to be expected; government meeting on economic issues, 03/23/26

- Kremlin.ru: Vladimir Putin held a meeting on economic issues, March 23, 2026

- TVP World, Tymon Miller: Rising oil prices bolster Russia’s war funding. New report from the Stockholm International Peace Research Institute (SIPRI); 03/23/26.

- European Leadership Network; Sinikka Parviainen; Senior Economist, Bank of Finland Institute for Emerging Economies: Understanding Russia’s wartime economy and why it matters for Euro-Atlantic security, March 20, 2026

- Peace Research Institute Oslo, PRIO; Pavel K. Baev: Moscow calculates benefits of Gulf conflict, coming short, March 17, 2026

Forecasts:

- German Institutes: Joint Economic Forecast: April 1, 2026

- BOFIT: BOFIT Forecast for Russia, March 30, 2026

- vz-nn.ru: The Ministry of Economic Development will lower its forecast for Russian GDP growth in 2026; March 28, 2026

- OECD: OECD Economic Outlook, Interim Report March 2026 – Testing Resilience, March 26, 2026

- de.euronews.com; Doloresz Katanich with AFP: OECD lowers eurozone growth forecast due to rising energy prices, March 26, 2026

- IEF RAS: Quarterly GDP Forecast. Issue No. 69, 03/16/26; Nezavisimaya Gazeta; Mikhail Sergeev: Russians do not believe in a peace agreement for Ukraine. According to survey participants, the economy’s toughest times are still ahead, March 17, 2026

Monthly and weekly economic reports:

- Politkom.ru; Marina Voitenko: Weekly Economic Report: Compromise Under Pressure from Uncertainty, March 28; Extremely High Volatility in Oil Prices and Extreme Uncertainty Regarding the Consequences, March 19, 2026

- Economic Expert Group: Economic Analysis March 2026, March 25, 2026

- CMASF Monthly Report: “Analysis of Macroeconomic Trends,” March 24, 2026

- Sergej Blinow: Macro Overview No. 12 (2026), March 24, 2026

- VEB Institute: Global Economy and Markets, Weekly Report

Industrial Production in February 2026:

- Finmarket.ru: Industrial production in Russia fell by 0.9% in February, March 25, 2026

- Kommersant; Artem Chugunov: Industrialists are not expecting the best. Industrial production in February and results of current business surveys, March 26, 2026

- Hard Numbers: Industrial Production in February: Below Trend, March 25, 2026